Sharp growth for worldwide trade in pastes in 2019/2020

It is no secret that the consumption of tomato products increased significantly in 2019/2020. This is definitely the impression that was given by the spectacular acceleration of retail sales recorded last spring in the aisles of many supermarkets around the world, leading to the almost total absorption of stocks everywhere in the world even before the start of the 2020 season.

As premature or hasty as it may be, this conclusion is based on a clear observation: the world trade in pastes grew last year by nearly 5% compared to its average level over the three previous years, confirming the results of previous observations that were commented in our articles published in December 2019 and April 2020. Over this last marketing year, the increase in quantities exported around the world by the tomato paste sector can be estimated at more than 153,000 metric tonnes (mT), of which a large proportion was shipped just during the two-month period of March-April 2020 (see our article on the acceleration of imports).

This acceleration most directly concerned concentrated purees and processed products intended for home consumption (due to the containment measures imposed around the world), leaving aside products specifically intended for out-of-home catering (see our various articles devoted to the CoVid-19 pandemic). However, the commercial upturn was further confirmed by the notable increases also recorded for the world trade in the canned tomatoes and sauces categories. For the first of these, the quantities shipped in 2019/2020 (1.868 million metric tonnes of finished products) increased by more than 7%, a jump that is unprecedented in recent times of some 130,000 tonnes of finished products compared to the period running 2017-2019. At the same time, worldwide trade in the sauces category, which has peaked just under the 1.4 million mT mark in recent years, found a new lease of life last year with an increase of nearly 6% and almost 80 000 mT compared to the average of the three previous years.

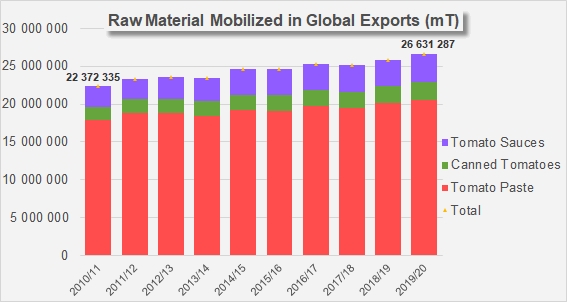

Ultimately, with more than 26.6 million mT of raw material equivalent* absorbed by global exports, the 2019/2020 marketing year marks a significant if not decisive increase of nearly 1.2 million mT (4.6%) against the average level of operations for the three previous years (2016/2017, 2017/2018 and 2018/2019). This result is among the most significant increases of the past decade.

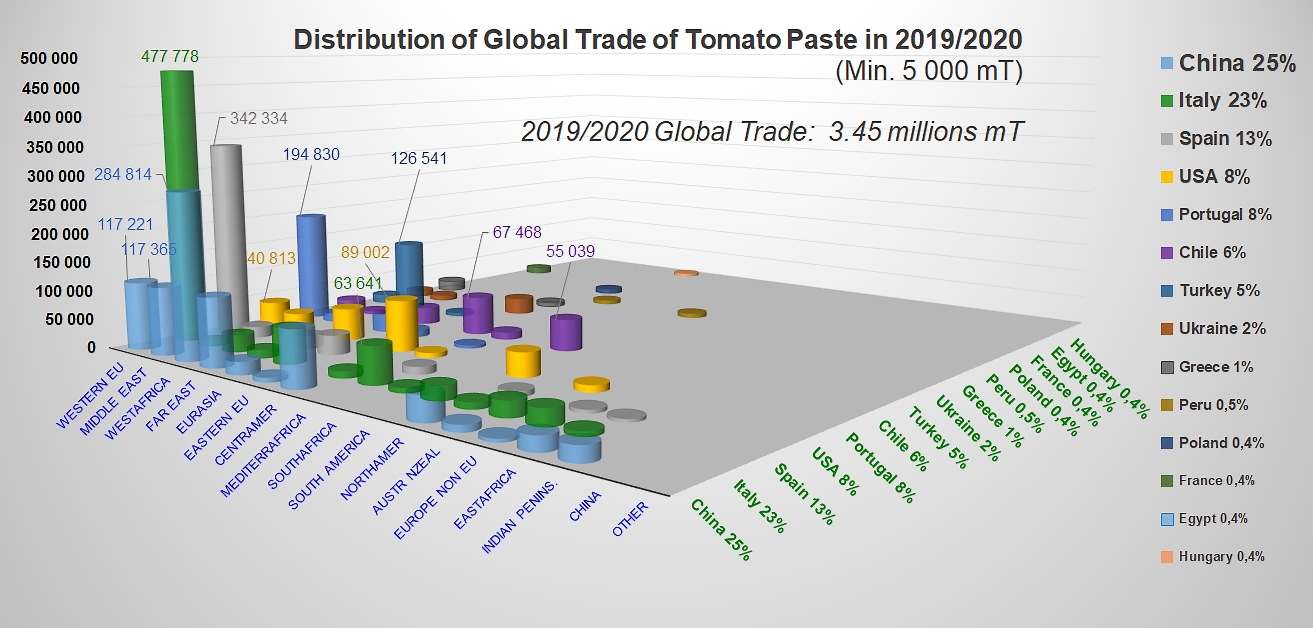

Tomato pastes: a rebalancing of forces

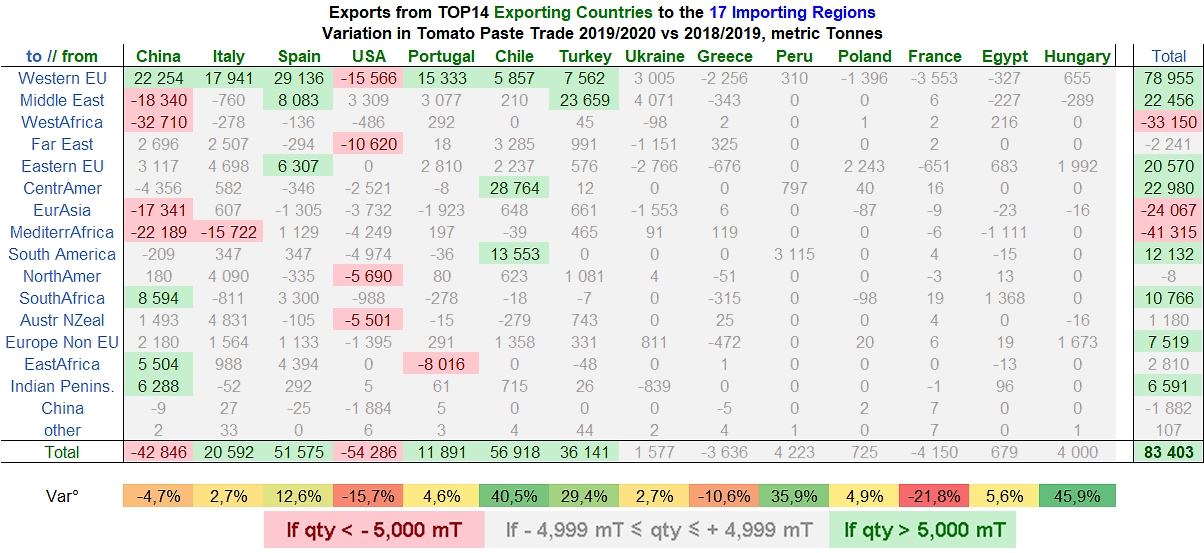

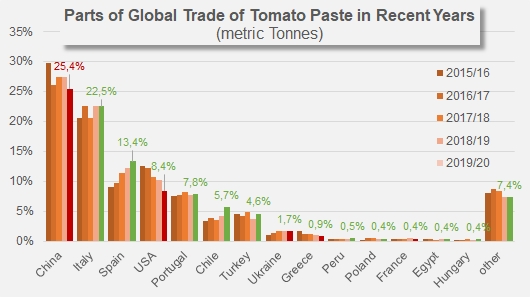

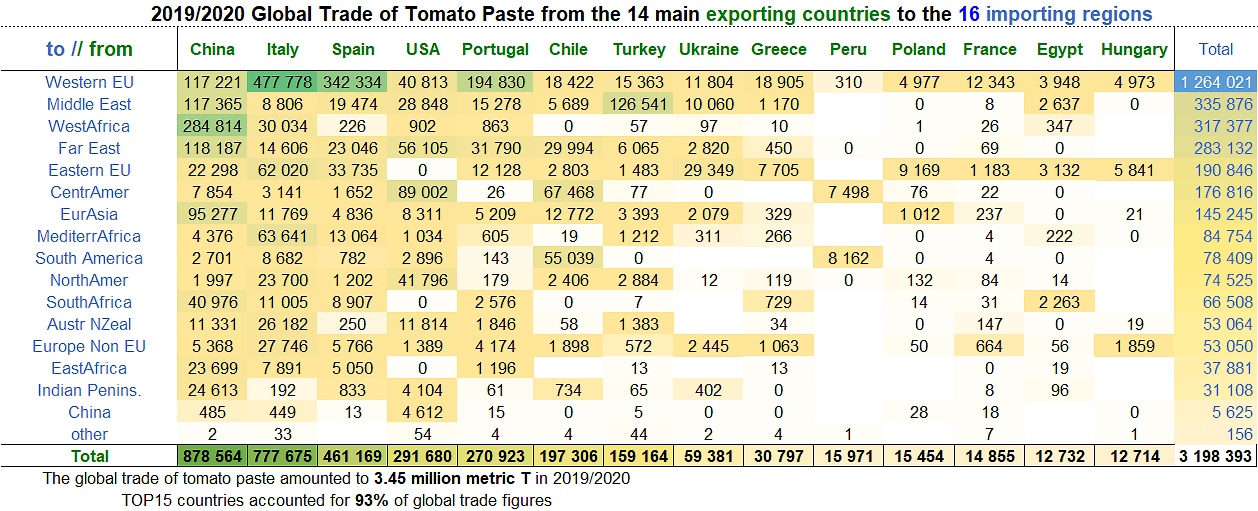

Against this general upward trend, from which a certain number of emerging industries (Ukraine, Peru, Hungary, etc.) have been able to take advantage, China and the United States once again recorded downturns in their foreign activities. Although the decline in Chinese exports remains relatively moderate (a little less than 43,000 mT of finished products, -4.7%) and differs only slightly from the average level of export operations during previous years, it is however considerably more significant for the US industry, whose performance fell by more than 54,000 mT against results for the 2018/2019 marketing year and nearly 75,000 mT (more than 20%) compared to the average for the three previous years.

With just under 879,000 mT of finished products exported in 2019/2020, Chinese operations have clearly borne the brunt of the significant reductions in purchases from Russian, Turkish, Algerian, Saudi, Emirati and Nigerian buyers, to mention only the main markets affected by the decline. Conversely, notable developments were recorded for shipments to Sudan, India, Angola and Mozambique, and Italy, but on a scale (around 52 000 mT in total) that has not been sufficient to offset the effects of the slowdowns (-95 000 mT in total) recorded for the usual main outlets.

For US products, the downturn affected virtually all outlet regions to varying degrees. However, unlike the objective reductions in imports observed for a number of the Chinese outlets, many of the regional destinations served by US operators have recorded more of a reorientation of their supply sources. This has been the case for the Western EU, as well as Central America, North America, etc. Among the most significant decreases, it is important to mention those that affected trade with Italy, Costa Rica, the Philippines, Canada, Turkey, Japan, etc. On the other hand, increases (+3 300 mT in total) were recorded on the Mexican, Malaysian, Emirati and Russian markets, but they remained overall fewer and above all too modest to compensate for the general decline (-57,600 mT). In total, the US industry exported less than 292,000 mT of tomato pastes in 2019/2020 (see the summary tables in the appendix at the end of this report).

Five national industries significantly improved their foreign results during the 2019/2020 marketing year. They are also those who made the most of the acceleration effect of the CoVid pandemic in March and April 2020. In this group, which also includes Spain, Turkey, Italy and Portugal, Chile's processing industry is the one that recorded the most spectacular progress last year. With nearly 200,000 mT of concentrated purees exported in 2019/2020, the Chilean result increased by around 40% (57,000 mT) compared to the previous marketing year and by 69,000 mT compared to the average performance of the past three years. Three regions (Western EU, Central America and Latin America) have been particularly effective drivers for the development of Chilean products, which moreover recorded only insignificant declines (-336 mT in total) in a mere three regions. More specifically, the most remarkable increases were recorded for sales to Argentina, Costa Rica, Japan, Italy, Cuba, Haiti, the Netherlands, Russia, etc.

The most notable nominal declines in Chilean foreign operations did not exceed 3,000 mT and were recorded for Greece, South Korea and Turkey.

In third place among worldwide exporters of tomato pastes, Spain confirmed its upward momentum over the 2019/2020 marketing year, a pattern that has been steadily progressing since the 2012/2013 marketing year. With the help of the CoVid effect, Spanish exports performed particularly well in countries of the EU as a whole (Netherlands, Portugal, Germany, United Kingdom, Poland, Croatia, etc.), the Middle East (Oman, Saudi Arabia), and East Africa (Sudan), and thus increased by more than 54,000 mT compared to the 2018/2019 marketing year. Overall, setbacks (-2,500 mT in total) were few and very limited, the most important one being recorded for deliveries to the Italian market. All in all, Spain posted an export result of 461,000 mT for 2019/2020, up more than 51,500 mT (+13%) compared to 2018/2019 and more than 93,000 mT (+25 %) against the average result for the three previous years.

The increase in Turkey's operations compared to the previous marketing year (+29%) is hardly less remarkable than that of Chile. However, the focus of Turkish foreign activity on a smaller commercial sphere than those of the countries already presented gives a strong contrast to its annual variations, which mainly concerned the Middle East and the Western EU, thanks to a sharp increase in deliveries to Iraq (+24,000 mT), Saudi Arabia (+2,800 mT) and Germany (+5,000 mT), and despite a sharp decrease to Syria (-3,000 mT). With the exception of two minor downturns in East Africa and South Africa (-55 mT in total), Turkish foreign operations increased on all the markets served, for a total volume of exports close to 160,000 mT, an increase of 36,000 mT against the 2018/2019 result.

As for Italy, the world's second largest exporter of concentrated purees, the 2019/2020 result may seem relatively modest compared to the previous year. The overall increase in the sector's exports barely exceeds 20,500 mT of finished products (+2.7%), for a nonetheless impressive total of around 777,700 mT. The very European orientation of Italian foreign operations is illustrated in the geography of the progress recorded over the latest marketing year. The most decisive gains were recorded in countries of the Western EU (Germany, the Netherlands, Belgium, Austria, etc.), the Eastern EU (Hungary, Romania, Czech Republic) and countries of non-Community Europe (Switzerland). Australia, Canada and Japan also contributed to the improvement in the Italian result, the only real decrease having occurred on the Libyan market, which is known to be extremely volatile in terms of quantities and sources. Finally, it is important to note that the Italian result for 2019/2020 shows an increase of more than 54 000 mT of finished products (+7.5%) against the average level of operations over the three previous years.

With an export result for the past marketing year of 271,000 mT, the performance of Portugal, the world's fifth largest exporter of the paste sector, combined on the one hand a spectacular drop in deliveries to Sudan, Russia and Oman, with on the other hand, a significant but contrasting increase in exports to countries of Europe in general (EU and non-EU), with notable increases for Italian, Spanish, Polish and Swedish buyers, and marked declines on the British, German and Dutch markets. This has resulted in a clear but moderate increase compared to the 2018/2019 marketing year (a little less than 12,000 mT, or 4.6%) and compared to the three previous years (a little more than 10,000 mT), but modest compared to those of neighboring countries.

The overall total progression of the other seven countries of the TOP14 list of exporters of concentrated purees on a global scale represents a little less than 3,500 mT of finished products, without much impact on the overall market profile. Significant declines affected Greek and French results, in particular due to a reorientation of supplies for several EU markets. Conversely, Ukrainian operators recorded an increase in their foreign sales thanks to the growth in demand from countries of the Western EU, the Middle East and non-EU Europe. Peruvian exports grew significantly thanks to orders from South America. The Eastern EU has proven to be a growth region for Poland, Egypt and Hungary, with the latter two countries also performing well on the Kenyan and Serbian markets respectively.

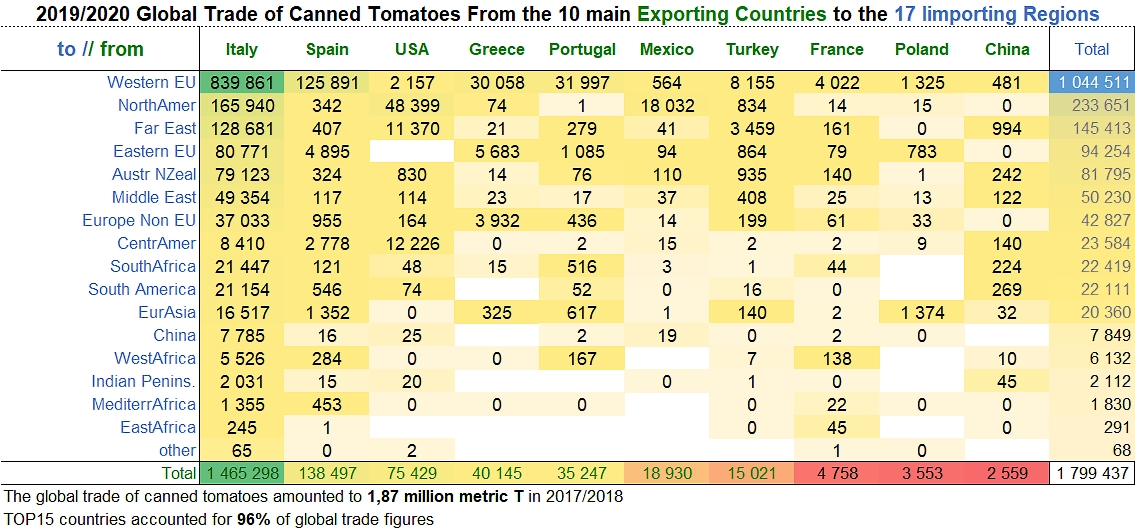

Canned tomatoes: increase in the proportional importance of top performers

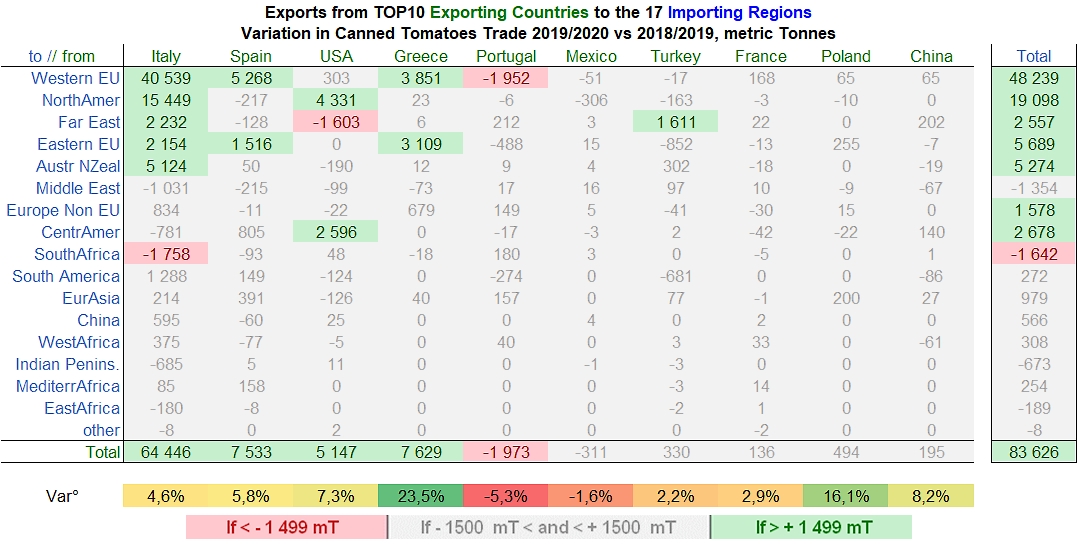

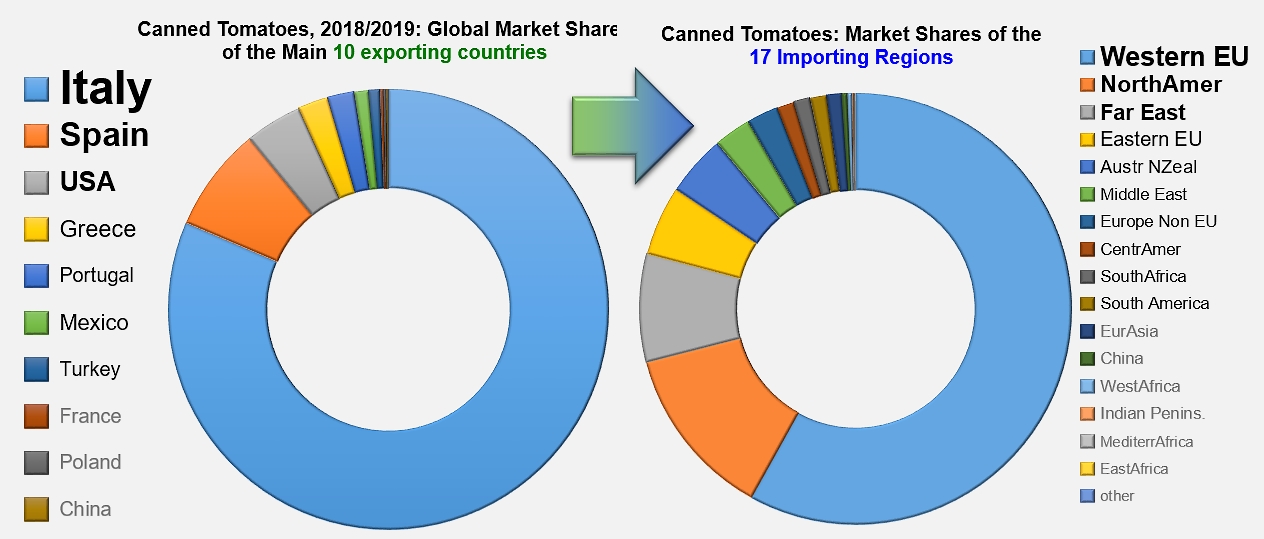

The 2019/2020 marketing year did not bring any change in the composition of the group of ten countries that lead the world's market for canned tomatoes. Beyond a few minimal changes in the ranking of the members of this group, which accounts for more than 96% of world supply, this marketing year even increased the weight of four of the five main countries operating in this category, in a context of significant increase on the global level. Indeed, the foreign sales of processing countries mobilized last year quantities that were 85,000 mT (4.8%) greater than the previous year, exceeding by 130,000 mT the average level of operations of the three previous marketing years (2016/2017, 2017/2018 and 2018/2019).

In the last marketing year, 1.87 million mT of canned tomatoes destined for foreign countries left the warehouses of processing plants, including 1.46 million mT shipped by the Italian industry alone. Italian operators relied on their usual major outlets (Western and Eastern EU, North America, the Far East and New Zealand) to develop their export activity, with the most significant increases occurring for shipments to the United Kingdom, USA, France, Australia, the Netherlands, etc. A few classic destinations, on the other hand, reduced their purchases of Italian canned tomatoes. The most significant contractions were recorded on the markets of Germany (-6,900 mT), Greece (-4,300 mT), Saudi Arabia and South Africa. All in all, the Italian performance improved in 2019/2020 by more than 64,000 mT compared to the previous year and by more than 104,000 mT (+7.7%) compared to the average level of activity for the period running 2016/2017-2018/2019.

Contrary to what has been observed occasionally for the tomato paste category, the year 2019/2020 did not record any big changes to the ranking of the destinations and regions of consumption of canned tomatoes. This stability and the increase in demand have enabled Spain, the category's second largest operator with 7% of world trade last year, to increase its sales on both markets where it can claim a certain level of competitiveness with Italy, the undisputed leader in the sector (78% of global sales), namely the Western EU and the Eastern EU. The most significant increases were recorded in sales to the United Kingdom, the Netherlands, Germany and Estonia, with a total increase that reached more than 8,300 mT of finished products, while the accumulated decrease, recorded in particular for Portugal and Greece, did not exceed 800 mT. The result for the Spanish canned tomato production sector (138,500 mT exported) is a 6% increase compared to 2018/2019, with a progression of 10,200 mT (8%) compared to the average of the three previous years.

As for the United States, third-ranking world operator of the canned tomato sector with 4% of trade in 2019/2020, the country took advantage of the increase in demand and, like Spain's performance within its immediate commercial sphere, increased foreign sales to North- and Central American customers (Canada, Mexico, Costa Rica, El Salvador, etc.). The past marketing year, which also recorded a decline in sales to South Korea and Malaysia, saw US exports increase by nearly 5,200 mT (+7%) compared to 2018/2019, to the point of exceeding 75,000 mT, which is approximately 11% more than the average of the previous three years.

Greece, whose purchases of canned tomatoes from the Italian and Spanish industries logically fell sharply in 2019/2020, also developed its exports to its usual markets of the European Union. The United Kingdom, Poland, Belgium, the Czech Republic and Norway significantly increased their imports of Greek canned tomatoes last year, and the few anecdotal declines in French or Dutch purchases in this category remained insufficient to affect Greek export dynamics. In the final count, more than 40,000 tonnes of canned tomatoes were exported by Greek companies, an increase of almost 7,700 mT (+23%) compared to the previous year and of more than 6,000 mT (+17%) against the average of foreign sales over the three previous years.

Portugal was virtually on par with Greece last year in the canned tomato export category, with a total of over 35,000 mT shipped abroad. However, unlike Greek exports, results for the year were down nearly 2,000 mT compared to 2018/2019, the difference resulting from significant slowdowns recorded for British, German, French, Greek and Polish purchases, which were not compensated by the increases recorded for Italian or Spanish purchases.

The marked polarization of this sector around Italian operations and the extremely small group of countries that “monopolize” more than 96% of world trade relegates into the background the results of Mexican, Turkish, French, Polish or Chinese operators. In 2019/2020, the accumulated activities of these few countries only amounted to a little less than 45,000 mT of finished products (less than 2.5% of global exports), and variations in their operations compared to the previous year did not exceed 170 tonnes. However, the increase in Turkish canned exports to the Japanese market deserves a mention.

The second part of this dossier will be published very shortly.

Some complementary data:

* : All estimates of equivalence with raw materials are based on recently revised official coefficients provided as appropriate by national industries or by TomatoEurope.

Performance of the major paste exporting industries by destination regions in 2019/2020

Performance of the major canned tomato exporting industries by destination regions in 2019/2020

Performance of the major ketchup and sauces exporting industries by destination regions in 2019/2020

Full detail tables of exports for each of the sectors mentioned in this report are available on request from the editorial staff of Tomato News: fxb@tomatonews.com

Find all the topics published under the tag "Trade, statistics, Consumption" by entering the keyword "trade" in our fast and/or advanced search module for articles.

Source: Trade Data Monitor LLC