World trade 2021/2022 (May-April): Covid continues to have an impact

Despite a slight annual decline, the quantities traded are significantly higher than pre-Covid activity levels.

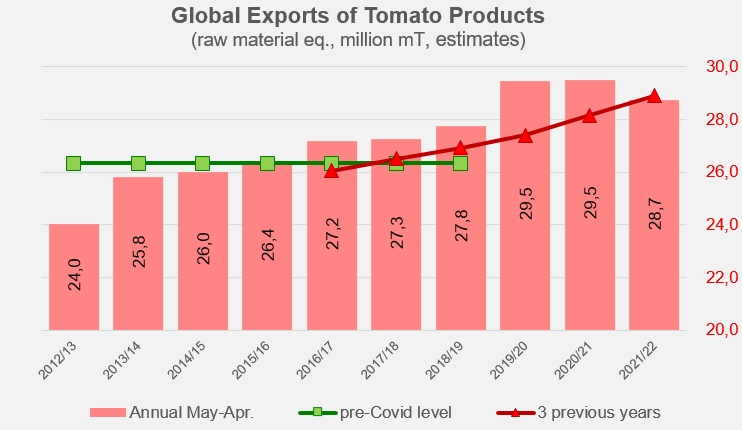

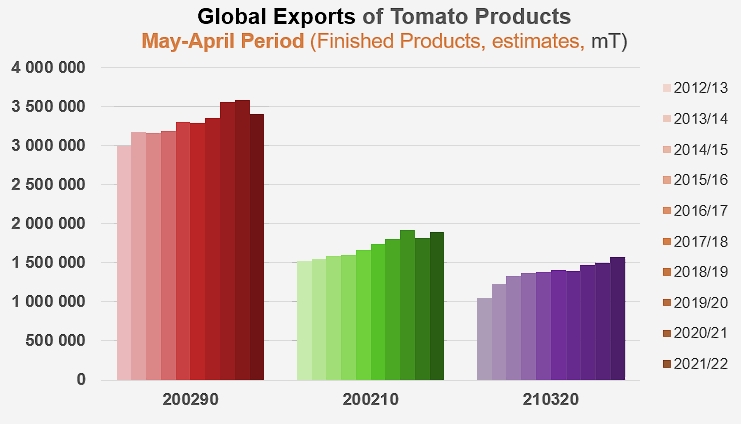

The 2021-2022 world trade in tomato products (studied over the period May 2021-April 2022 for reasons of data availability) confirmed the expectations of international market experts. Despite the slight increase in processed quantities (+2%) recorded between 2000 and 2021, available volumes have not fueled an increase in supply flows : after two years marked by an exceptional acceleration of global exchanges, in a context of extreme tension in the area of inventories (the two phenomena being closely linked and consecutive to the Covid pandemic), trade seems to have begun a gradual return to "normal levels", while remaining at a level clearly higher than those of the "pre-Covid" years.

A quick estimate of total exports (expressed in fresh tomato equivalent, all product categories combined) shows that overall activity over the May 2021-April 2022 period decreased by nearly 780,000 mT (-2.6%) from the previous period and by more than 180,000 mT (-0.6%) from the average of the previous three equivalent periods. However, the same results show that, conversely, world trade increased by 1.3 million mT (+4.8%) compared to the average level of the pre-pandemic period (May 2016-April 2017 to May 2018-April 2019).

This persistent high level of trade on a global scale masks major differences both in terms of product categories and in terms of the market shares of the major countries involved in the industry.

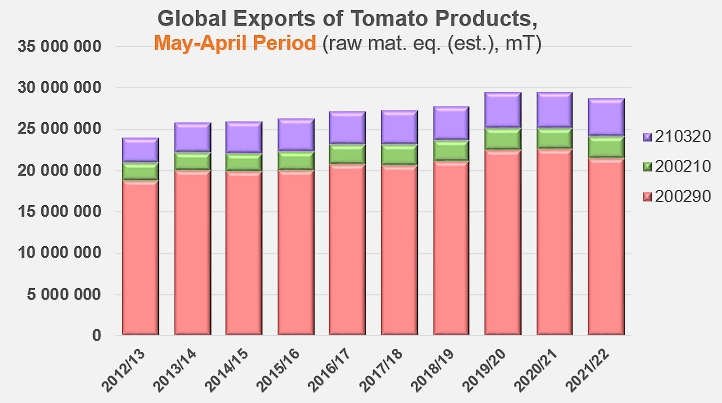

Over the period under review, the progress of the various categories has confirmed the results observed, in particular for the 2020/2021 marketing year, and which were commented in our last consumption study. The quantities mobilized for global exports of pastes (customs codes 200290) during the twelve months between May 2021 and April 2022 recorded a notable decline (-1.1 million mT or -5%) compared to the corresponding period of the previous year. But it would be premature to conclude that this indicates a decline in global needs or demand insofar as this 2021/2022 result shows at the same time an increase of 0.57 million mT (+2.7%) compared to the average pre-Covid level. In addition, other significant increases have been recorded in the other categories – canned tomatoes (customs codes 200210) and sauces and ketchup (customs codes 210320) – not only in relation to average pre-Covid levels but also in relation to the same period (May-April) of the previous year. These increases, which reached 4.6% for canned tomatoes and 5.6% for sauces respectively each year (and up to 9% and 13% compared to the three-year period prior to the pandemic) seem to confirm for the second year in a row the continued strong demand for at least two of the three tomato product categories considered.

(See additional information at the end of this article)

In the difficult agro-industrial context that the tomato processing sector has also experienced in recent years, particularly in terms of quantities harvested and processed, the dynamics at play seem to indicate that the slowdown in trade is more the consequence of difficulties encountered upstream in the sector, in terms of the availability of raw materials and products, than the manifestation of a change downstream in the sector, likely to be expressed by a decrease in consumer demand.

TOP12 paste trade flows: adjustments are ongoing

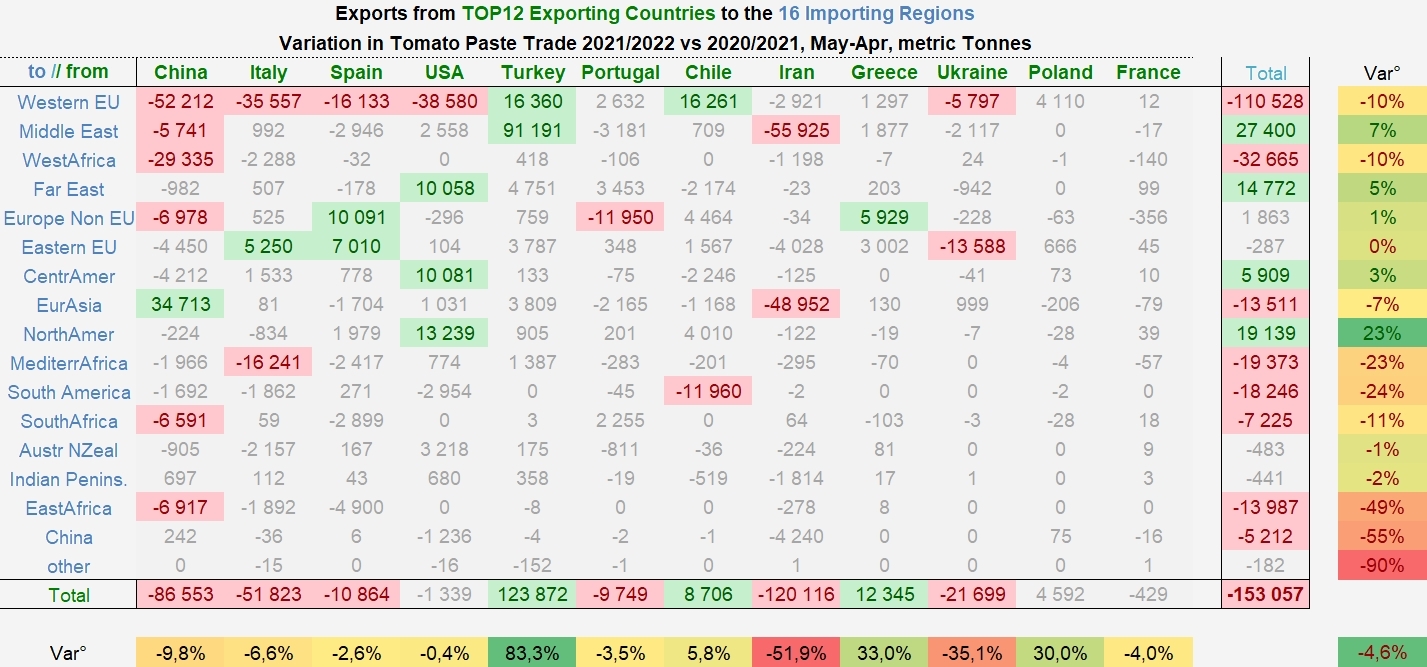

After two very intense years in terms of product movements, the slowdown in export activity of the TOP12 countries has been particularly felt in the Western EU (-10%), Western Africa (-10%), Mediterranean Africa (-23%), East Africa (-49%) and Southern Africa (-11%). South America (-24%), Eurasia (-7%) and a few others complete this group of regions whose total impact has resulted in a decline of some 220,000 mT. Conversely, some increases in foreign supplies can also be noticed over the same period, notably in the Middle East (+7%), North America (+23%) and the Far East (+5%). Overall, the quantities imported from the TOP12 countries amounted in 2020/2021 (May-April) to 3.19 million mT against 3.34 million mT over the same period of the previous year, i.e. a negative annual variation of around 4.6%.

The dominance of the TOP12 in the world paste trade has been slightly eroded over the past decade, with the proportion of the leading countries representing just over 93% of total trade in 2021/2022, compared to over 96% in 2012/2013.

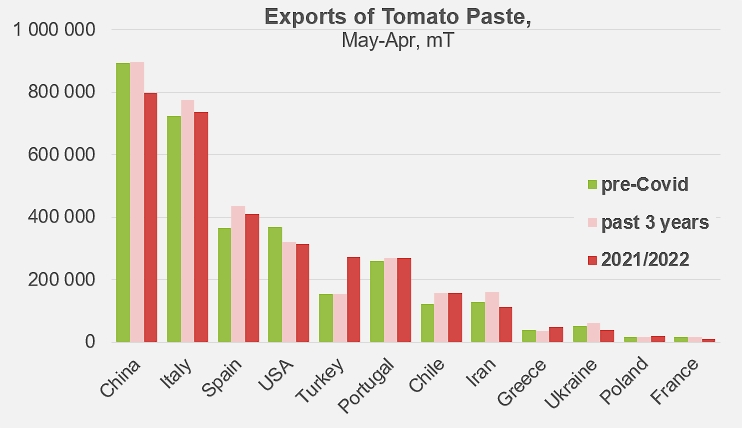

In this context of trade contraction, the results of the main countries involved in the sector have been very mixed. Two significantly active countries have weathered the crisis particularly well and made remarkable inroads into the world market: with nearly 273,000 tonnes of pastes (finished products) exported between May 2021 and April 2022, Turkish operators improved their result by more than 83%, compared to just under 149,000 mT in the corresponding period of the previous year, thereby reaching a historically high level of activity. Most of this progress was built on sales to Iraq (at the expense of Iranian products in particular), but also on exports to Italy, Oman and Syria. This latest Turkish result is also 78% higher than during the pre-Covid period (about 153,000 mT on average annually between 2016/2017 and 2018/2019 (May-April)).

As for Greek paste exports, they recorded an increase of about 33%, to nearly 50,000 mT over the period under review. This result, mainly recorded thanks to the British and Polish markets, brings Greek operations back to the levels recorded between 2012 and 2015 and to a level about a third higher than that of the three years prior to the Covid pandemic (38,000 mT).

Chilean paste sales also benefited over the period, improving their performance by almost 9,000 mT (+5.8%) compared to the same period of the previous year. A significant increase in exports to the EU (Germany, Sweden, Italy, Poland, etc.) compensated for a drop in trade flows to Argentina. The Chilean result shows an increase of 29% compared to the pre-Covid period (approximately 122,000 mT) (see our additional information at the end of this article).

The other major tomato paste exporting countries have all recorded declines in activity to varying degrees.

The most important one in terms of quantity is Iran, whose official export data shows a drop of more than 50% in annual variation, from 230,000 mT in May 2020-April 2021 to around 110,000 mT in May 2021-April 2022. The main components of this decline are the spectacular drops in sales to Iraq, the Emirates, Afghanistan, Russia and Romania. The Iranian result is 13% below its average pre-Covid level (127,000 mT).

With exports falling from nearly 900,000 mT to less than 800,000 mT, the Chinese sector recorded a counter-performance that brought its annual operations down to a level it had not seen since 2005/2006. The markets most affected by the slowdown have been European (Italy, Portugal, Poland), African (Nigeria, Togo, Congo (Dem. Rep.), Guinea, Angola, Sudan) and Middle Eastern (Yemen, Saudi Arabia, Israel), to name only the most notable. Despite a sharp increase in exports to Russia, the year's decrease amounted to some 86,000 mT, which is approximately 10% of China's result over the previous period. Quantities exported during the reference period were 11% lower than during the pre-Covid period (890,000 mT).

Italian results have not been particularly satisfactory either, with a negative annual variation of nearly 7% between 2020/2021 and 2021/2022 (May-April), essentially linked to the decline in exports to the western EU (Germany, France, the Netherlands, Austria) and Mediterranean Africa (Libya), which were not offset by the increases recorded, in particular to Poland. So total exports have fallen from nearly 790,000 mT to less than 740,000 mT, a level of operations that remains slightly higher than before Covid (approximately 723,000 mT).

The end of the pandemic period was less abrupt for Spanish exports, with official figures showing an annual decline of just over 2.5%, mainly recorded on the markets of the western EU (Italy, Germany, Portugal, Sweden, etc.), East Africa (Sudan), the Middle East (Saudi Arabia, Kuwait) and Libya. Conversely, there were notable increases in the quantities of pastes delivered to the United Kingdom and Croatia. Ultimately, the 410,000 mT exported by Spain between May 2021 and April 2022 places the latest result at 13% above pre-Covid activity levels (approximately 364,000 mT).

The decline recorded by Portuguese exports is almost equivalent in quantity to the one observed in Spain, but slightly more marked in proportion (-3.5%). The main markets affected were British, Omani, Kuwaiti and Russian. Increases were recorded in sales of products to Japan, South Africa and the Netherlands, so that with just over 268,000 mT exported, the Portuguese industry has nevertheless recorded a result 3% higher than that of the pre-Covid period (260,000 mT).

The quantities of pastes exported by the United States show only a minimal annual variation, going from just under 315,000 mT in 2020/2021 to close on 314,000 mT in 2021/2022. However, this apparent stability masks a drastic drop in sales to Italy, which has been offset by a few increases in foreign sales, notably to Canada, South Korea and Taiwan, as well as to South America (Mexico, Costa Rica, Guatemala and Colombia). As in the case of China and Iran, the US result also remains well below its pre-Covid level (around 368,000 mT).

Comparison of results for the baseline period (May 2021-April 2022) with the corresponding periods of the previous three years (2018/2019 through 2020/2021) and the three pre-Covid years (2016/2017 through 2018/2019).

Several EU countries (Italy, Spain, Portugal, Greece, and Poland) as well as Turkey and Chile show improved performances compared to the pre-Covid period, while Chinese, US, Iranian, and French results remain below this threshold.

Due to the situation in Ukraine since the end of February 2022 and the probable criminal appropriation of some Ukrainian products by Russian forces, the data presented can only be partially representative of the export dynamics of the Ukrainian industry during the reference period. For the period ending in February 2022, annual foreign sales (March 2021-February 2022) were 20% lower than during the corresponding period of the previous year and 9% lower than the average activity during the three years preceding the Covid pandemic (see our related articles below and the monthly trade reports published on our website www.tomatonews.com).

Some complementary data

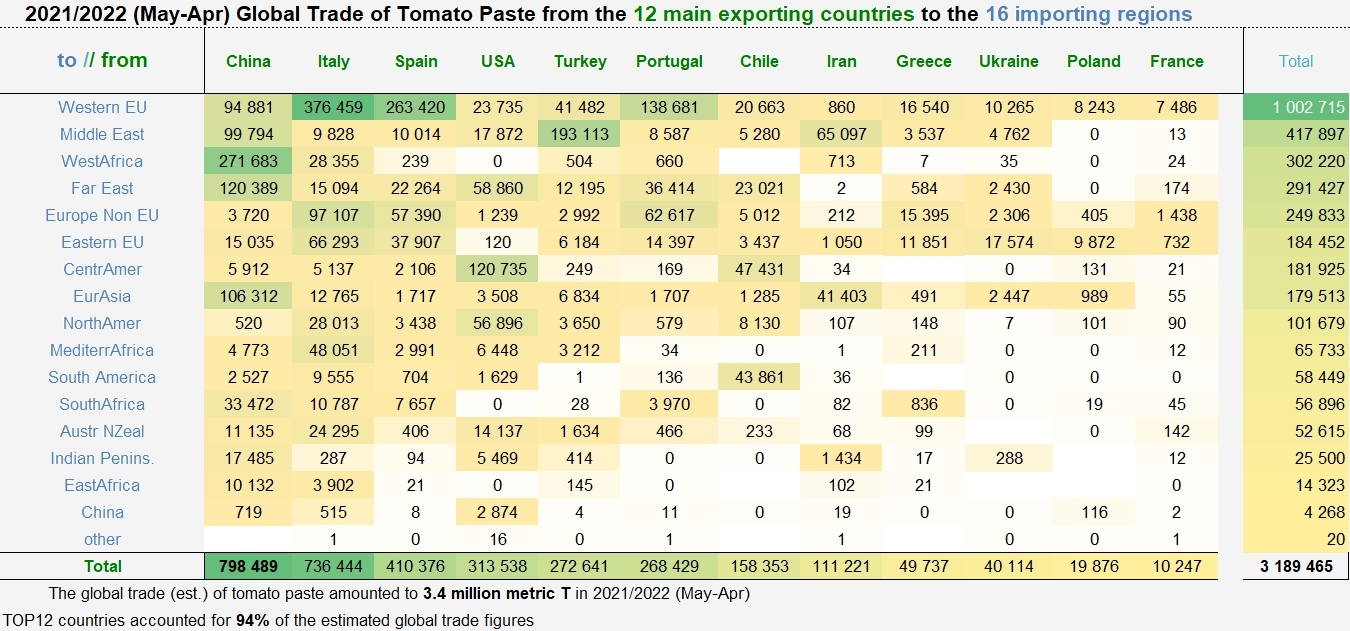

World exports of tomato products over the period May 2021 - April 2022.

Pastes (200290...)

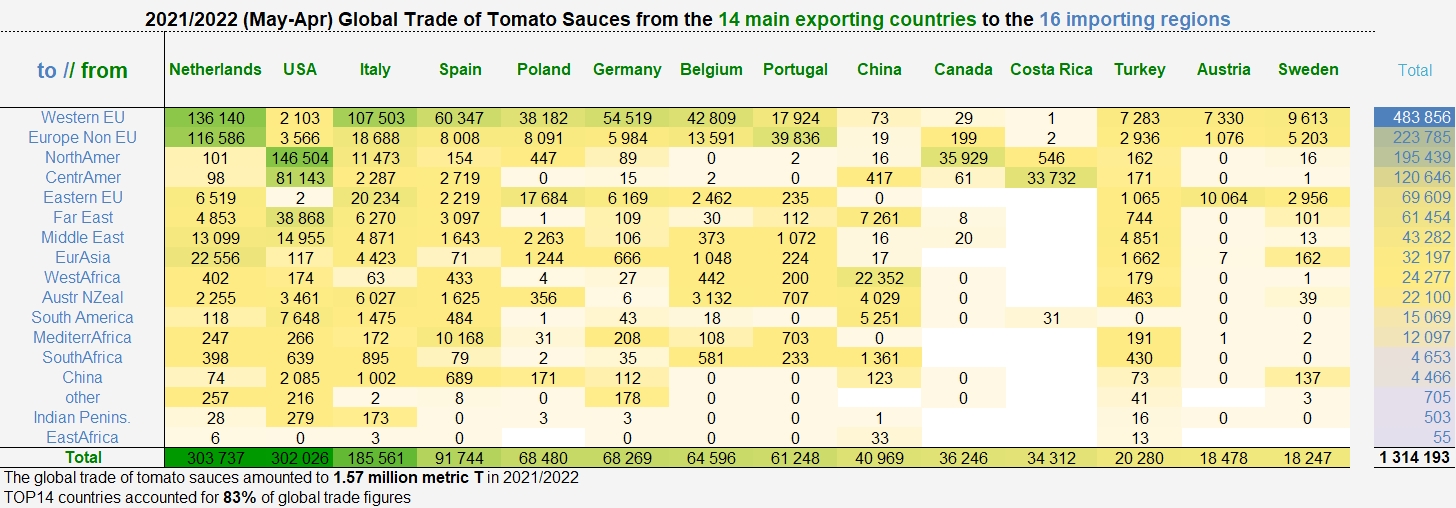

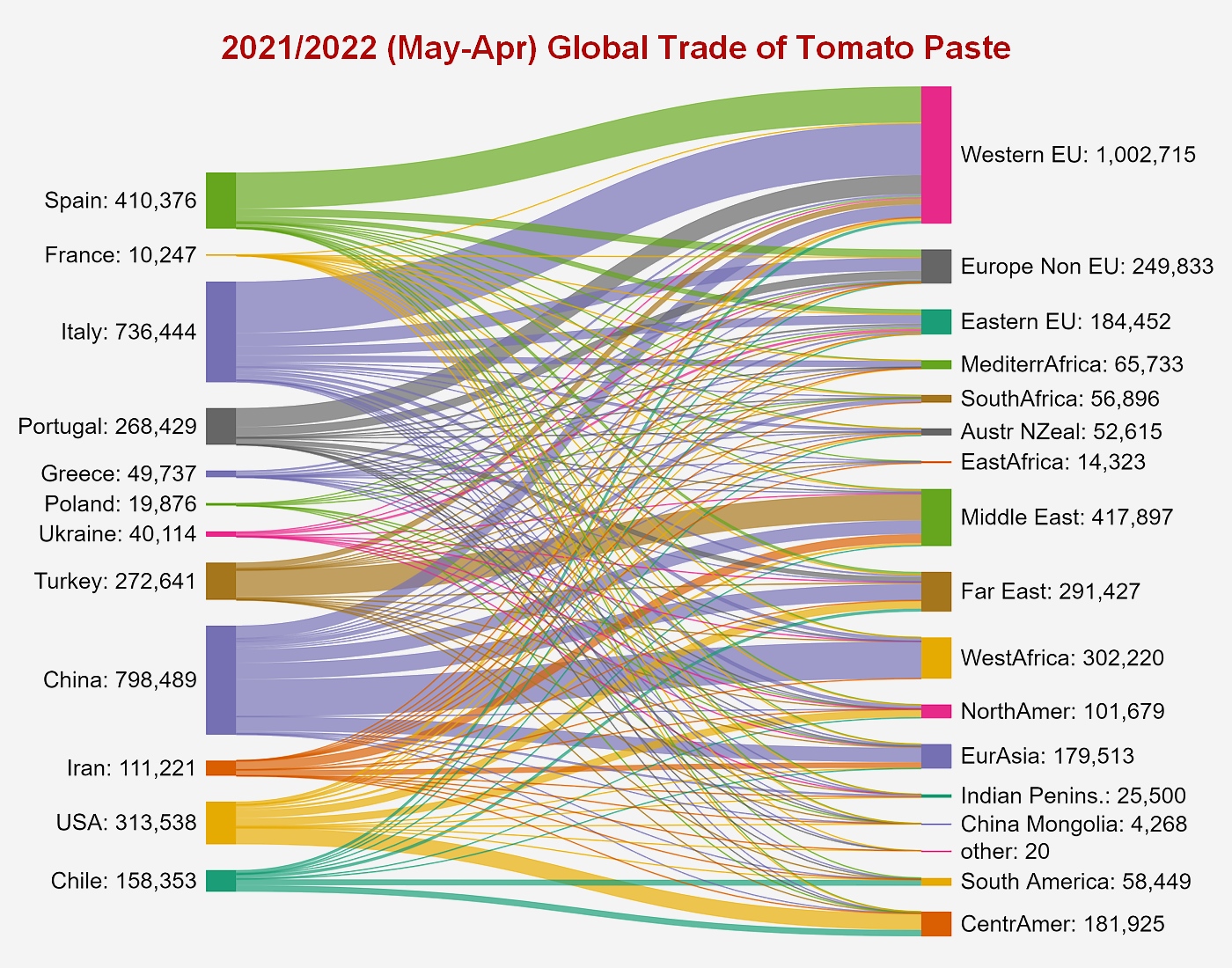

Quantities of tomato paste exported between May 2021 and April 2022 by the twelve main exporting countries operating in the category, to the sixteen importing regions (defined in 2011, revised in 2018).

Presentation of 2021/2022 tomato paste sales, for annual trade flows above 5,000 mT.

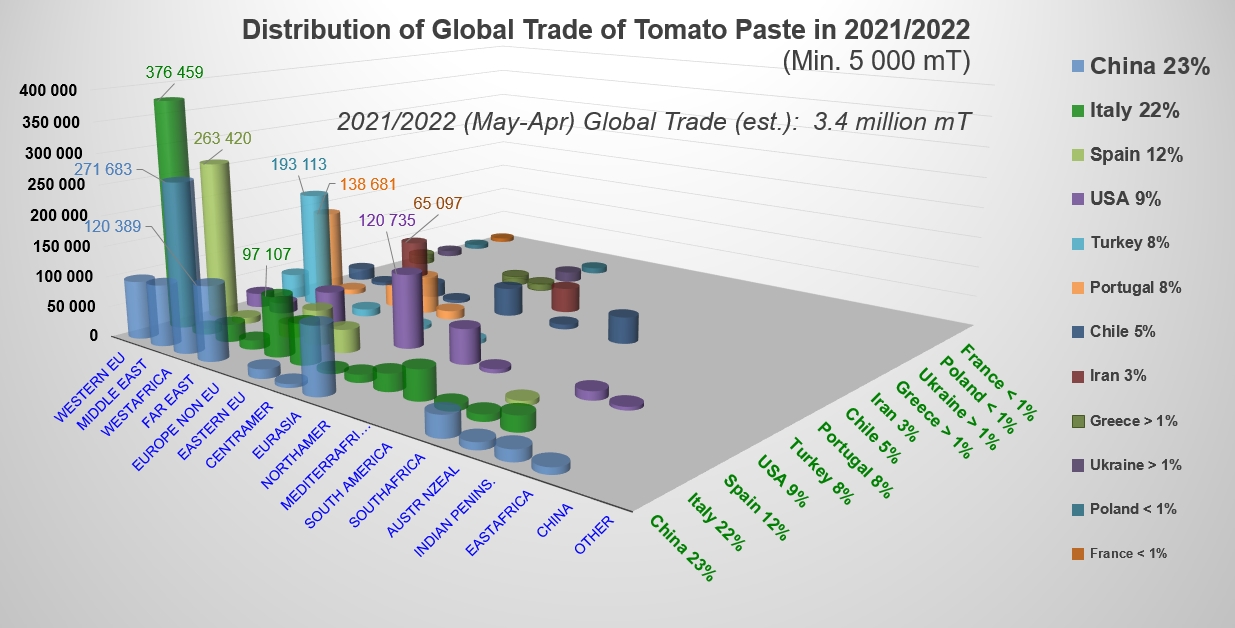

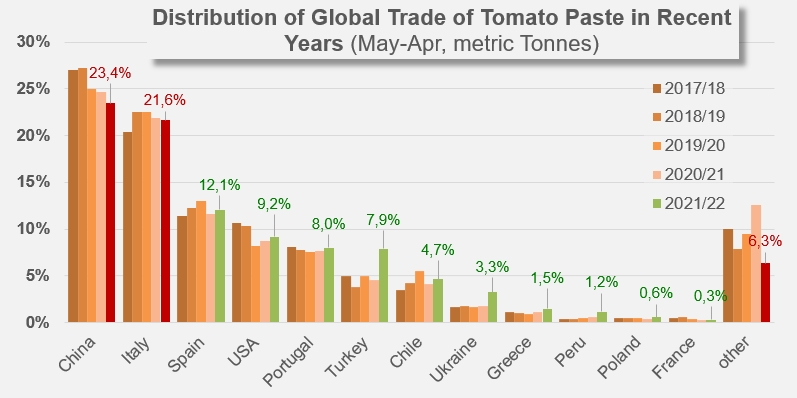

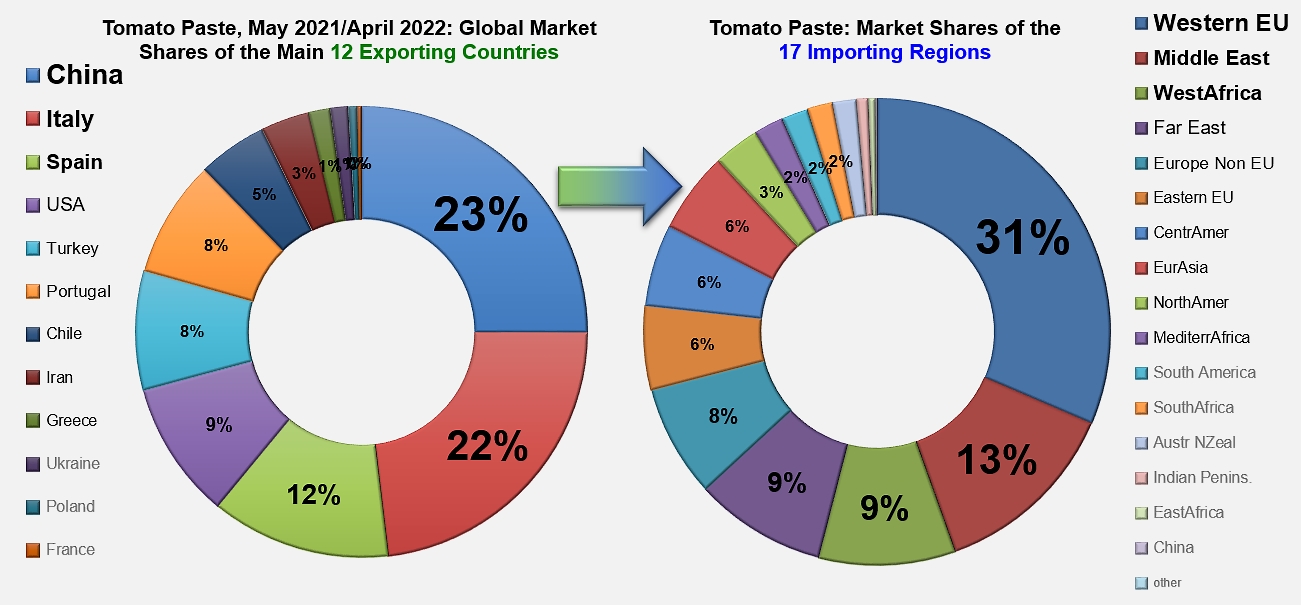

Recent evolution of the market shares of the twelve main countries involved in the tomato paste category.

Schematic representation of Tomato Paste (codes 200290..) exports over the period May 2021 - April 2022, from the 12 main exporting countries to the 16 recipient regions.

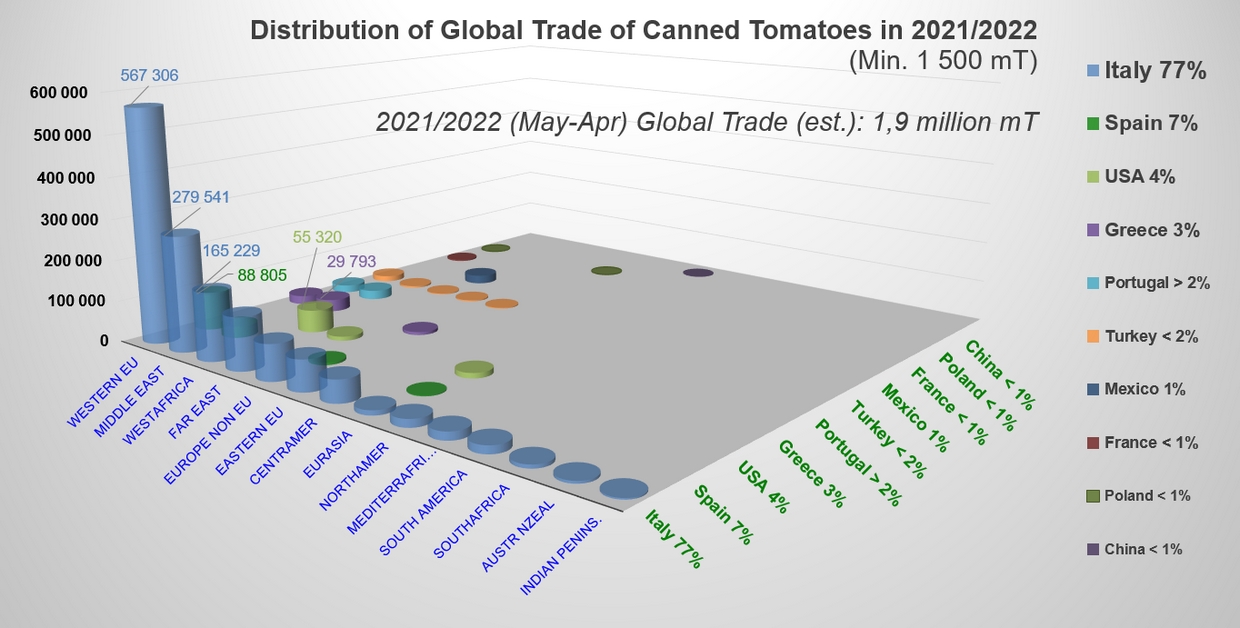

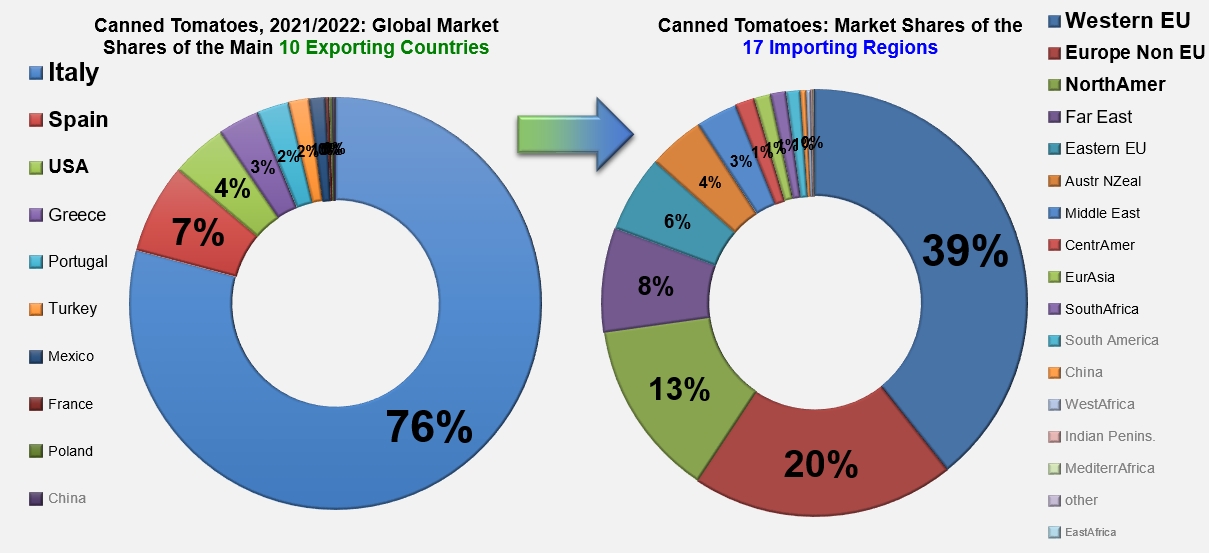

Canned tomatoes trade results for the TOP10: levels comparable to those reached at the height of the pandemic

Foreign sales of canned tomatoes (peeled, unpeeled, whole, cubed, etc., customs codes 200210) during the period running May 2021-April 2022 took place in a particularly buoyant context which, for the TOP10 exporting countries of the industry as well as for global movements as a whole, resulted in a significant increase of 4.6% compared to the previous year and 9% compared to the three-year period preceding the Covid pandemic. Quantities traded worldwide amounted to 1.897 million mT of finished products between May 2020 and April 2021, while they had reached the record level of 1.922 million mT at the height of the pandemic in 2019/2020.

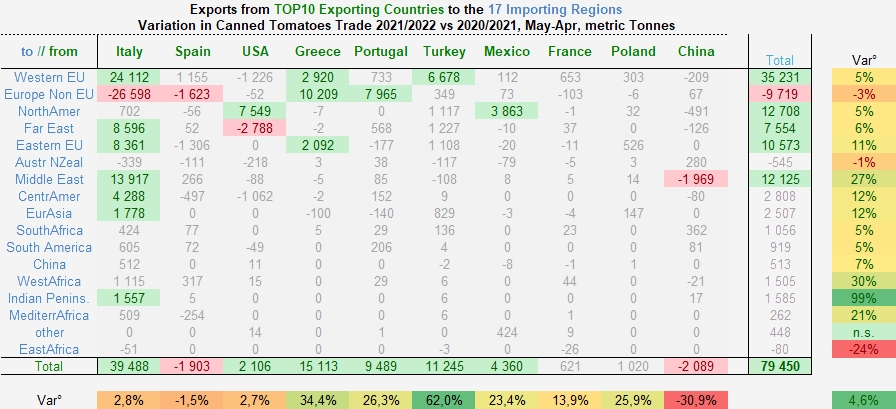

The acceleration has affected virtually all regions, with the exception of non-EU Europe, where the result was clearly influenced (-3%) by the sudden return of British imports to their pre-Covid level. For those regions that are usually large consumers of canned tomatoes (western EU, North America, Middle East, eastern EU and Far East), the most significant increases ranged from 5% to 27%, with world flows increasing by almost 80,000 mT.

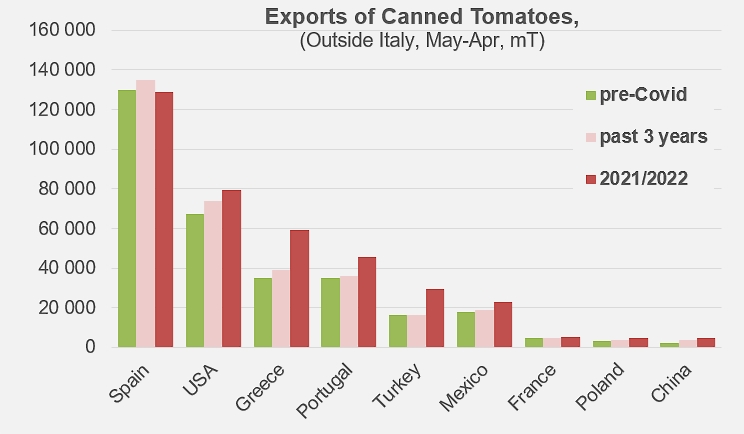

As in the case of the paste category, Turkey and Greece stand out for the intensity of the progression of canned tomato sales, which began during the Covid pandemic and continued beyond. These two countries have seen their foreign sales increase by more than 11,000 mT (+60%) and 15,000 mT (+34%) respectively, with Turkish canned tomatoes performing well on the Italian and German markets, and Greek products on the British market. This latter market also proved to be a buoyant one for Portuguese products, providing them with most of their annual growth (9,500 mT, +26%). Mexico is also among the countries that recorded strong growth between 2021 and 2022 (+23%) on smaller volumes (+4,400 mT, mainly shipped to the US market).

The annual variations recorded by the other important industries of the sector were of much more modest proportions. For their part, foreign sales of US canned tomatoes only increased by a little more than 2,000 mT (2.7%), against annual operations of around 78,000 mT. The Canadian market, historically its main outlet, largely contributed to the improvement in the US performance, but significant reductions in flows impacted sales of US canned goods to South Korea and several Central American countries (Honduras, El Salvador, Colombia, and Belize). In the final count, the latest US result shows an 18% increase compared to the average level of the pre-Covid period.

The exception to the general rule of growth is Spain, the world's second largest supplier, which recorded a very slight decline (-1.5%) of a few hundred tonnes over the year. In fact, none of the variations recorded in the seventeen regions supplied are particularly critical. The few decreases reported concerning Estonia (1,000 mT), the United Kingdom (1,800 mT), the Netherlands (1,300 mT), Italy (1,300 mT), and Belgium (1,100 mT), have been compensated by a net increase in products shipped to France (4,300 mT). Ultimately, Spanish exports of canned tomatoes are the only ones to show a result for 2021/2022 that is merely equivalent to that of the period before the pandemic.

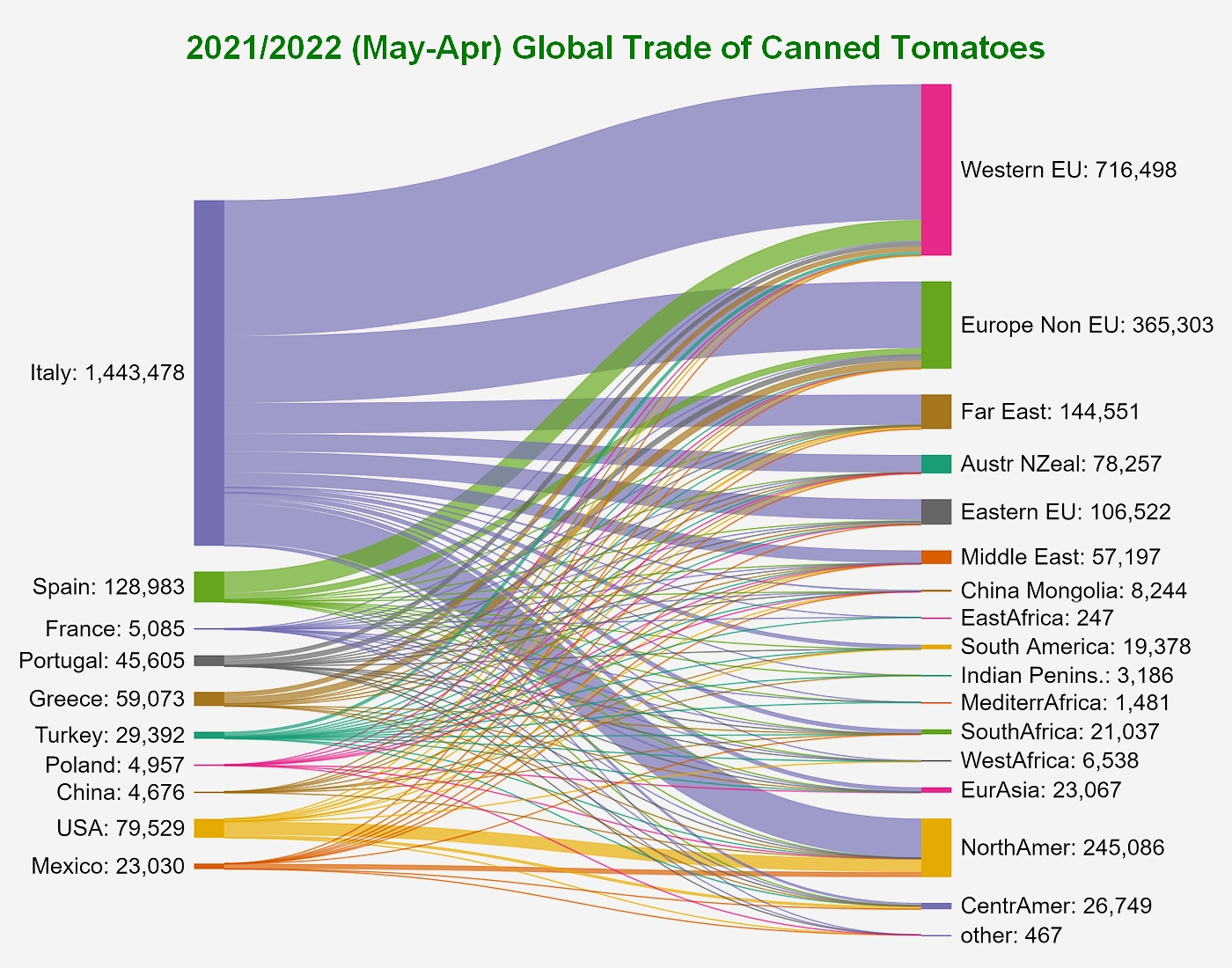

Despite the severe contraction of British supplies, significantly lower even than their pre-Covid levels, Italy has consolidated its position as the undisputed market leader and has alone contributed to almost half of the overall increase. In parallel with the fall in sales to the United Kingdom (-30,000 mT), the Italian industry has recorded several significant increases on the markets of the western EU (Germany, Spain, Belgium, Sweden, etc.), the Middle East (Saudi Arabia, Israel, Emirates), the Far East (South Korea), the eastern EU (Poland, Czech Republic), Central America, etc. With more than 1.44 million mT exported in 2021/2022 (compared to 1.4 million mT last year) and only 130,000 mT for its "immediate" challenger (Spain), the Italian sector signs its second best recorded performance and a result that is up 6% on pre-Covid levels of operations (see our additional information at the end of the article, our related articles below and the monthly trade situations published on our website www.tomatonews.com).

Comparison of results for the baseline period (May 2021-April 2022) with the corresponding periods for the previous three years (2018/2019 through 2020/2021) and the three pre-Covid years (2016/2017 through 2018/2019). For presentation reasons, Italian results are not shown on this histogram.

With the exception of Spain, whose results can be considered stable, all countries show a net increase in performance compared to the pre-Covid period.

Some complementary data

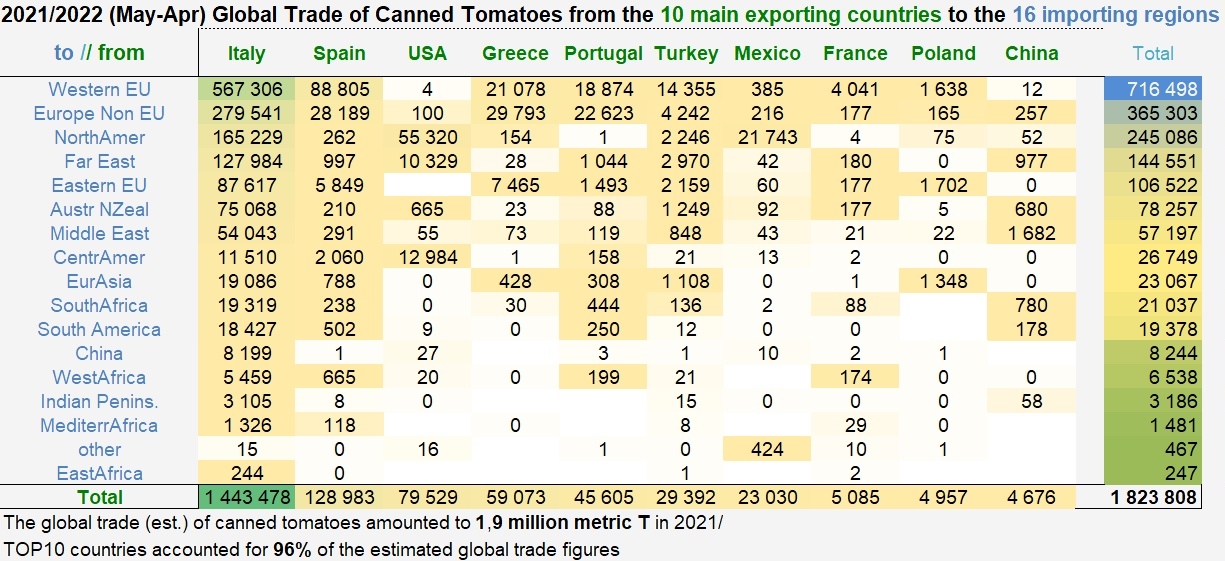

World exports of tomato products over the period May 2021 - April 2022.

Canned tomatoes (200210...)

Quantities of canned tomatoes exported between May 2021 and April 2022 by the ten main exporting countries operating in the category, to the sixteen importing regions.

Presentation of 2021/2022 canned tomato sales, for annual trade flows above 1,500 mT.

Schematic representation of Canned Tomatoes (codes 200210..) exports over the period May 2021 - April 2022, from the 10 main exporting countries to the 16 recipient regions.

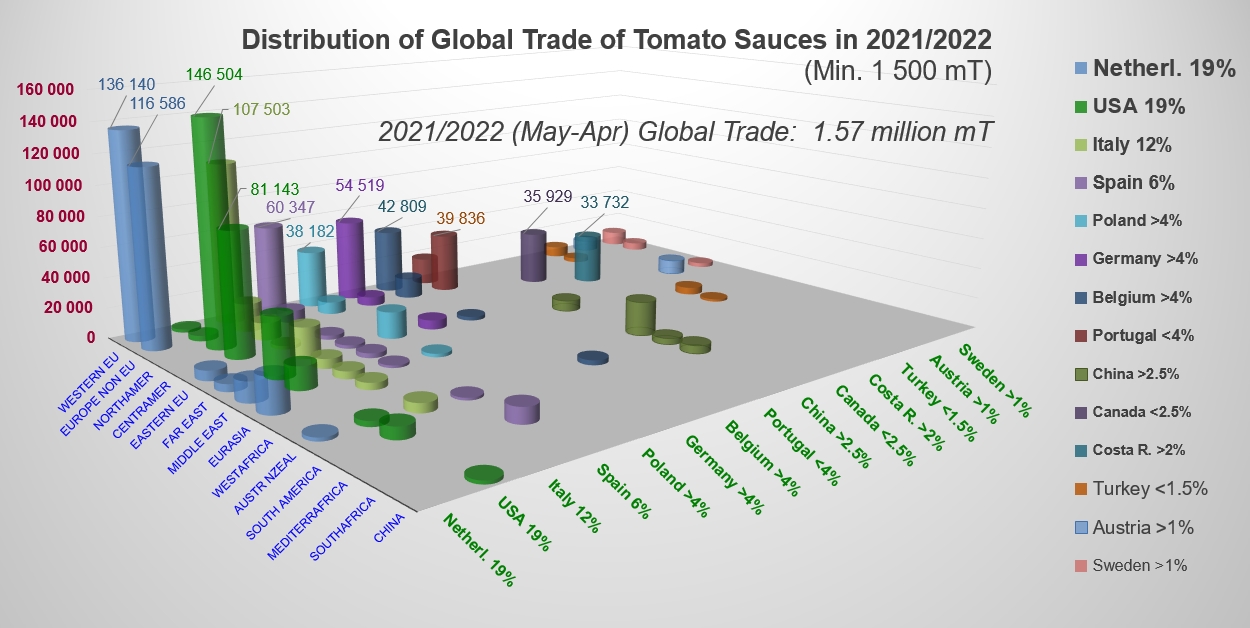

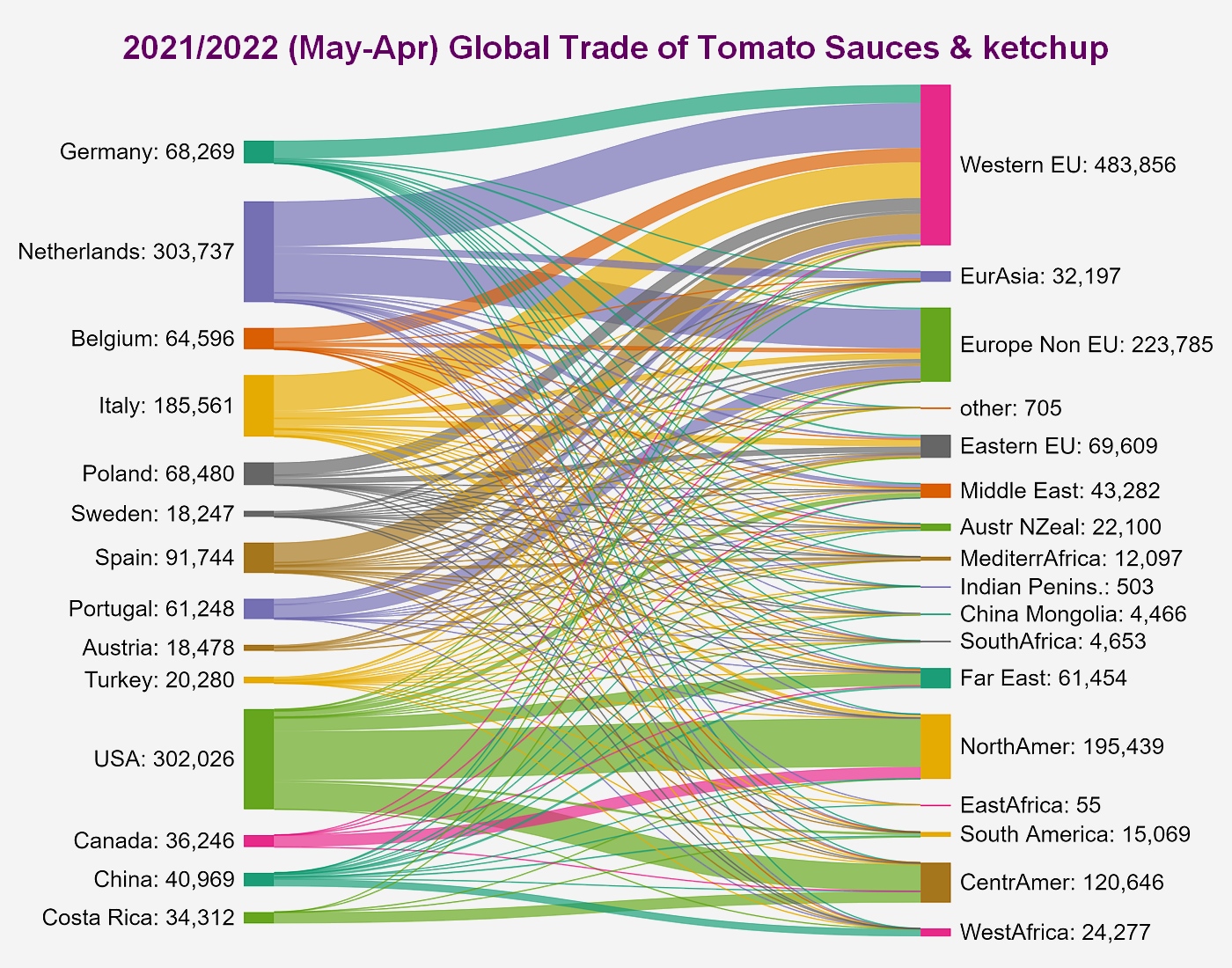

World trade for the sauces category: the boom in second-stage remanufacturing processing

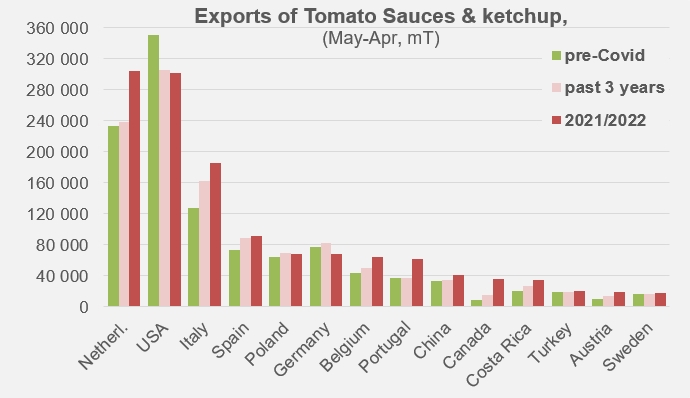

Over the period under consideration (May 2021-April 2022), the sauces and ketchup sector was more buoyant than the canned tomatoes sector, even more so for the leading countries (TOP14) in the industry than for world trade as a whole, and also more so compared to the pre-Covid period than compared to the previous year.

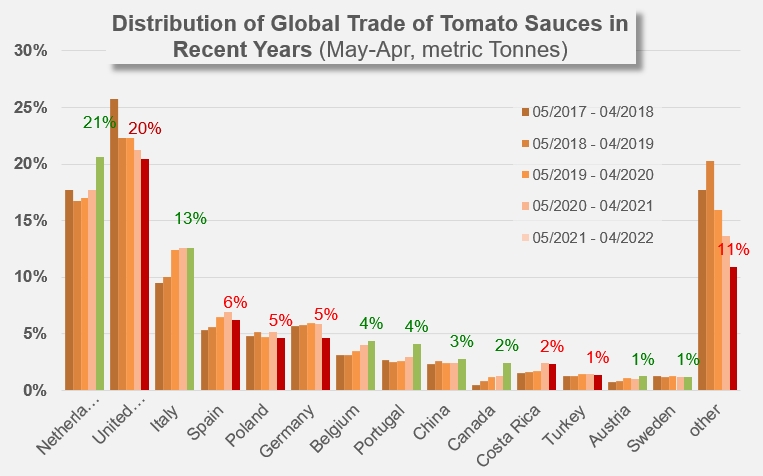

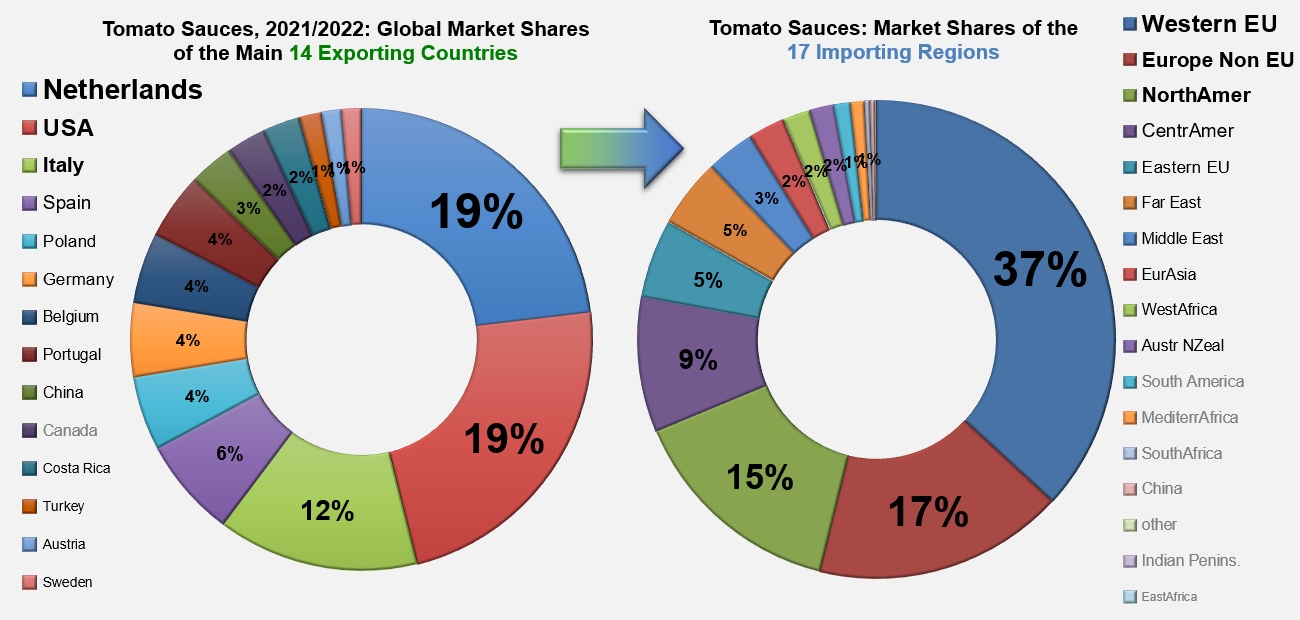

According to official statistics, trade in sauces and ketchup mobilized 1.57 million mT (finished products) in 2021/2022 on a global scale, compared to just under 1.5 million mT during the previous period. Furthermore, with another historical record result, the TOP14 countries alone supplied more than 83% of global shipments, a level far higher than the 80% recorded on average over the previous ten years.

With the notable exception of North America and a few regions with very low consumption figures (South and East Africa, China, the Indian Peninsula), all regions were particularly buoyant in terms of imports over the period under consideration, with an overall annual result of nearly 200,000 mT (+18%) more than during the period preceding the pandemic. Imports from all EU countries increased by nearly 100,000 mT, those from non-EU Europe and Central America by more than 37,000 mT each, those from Eurasia by nearly 23,000 mT, those from Mediterranean Africa by nearly 10,000 mT, etc. A notable exception to this list of countries whose results increased, Canada's supplies pursued their decline begun in 2015/2016, particularly from the United States, which conversely now appear to be an important outlet for Canadian sauces and ketchup production (see also our related articles below).

This year, the position of the world's leading exporter of sauces has been taken by Dutch operators from the USA, which had largely held it for many years: both countries virtually equaled each other over the period running May 2021 to April 2022, with some 304,000 mT of finished products exported by the Netherlands against a little over 302,000 mT shipped abroad by the USA. The volumes involved in this trade flow (a little over 19% of the world market for each of the two leading countries) reflect a spectacular increase of over 58,000 mT (+24%) compared to the previous year for Dutch products, while US foreign sales increased by nearly 8,400 mT and 3% compared to 2020/2021. Dutch growth was built on all its usual outlets (+32,000 mT for EU countries (Germany, France, Belgium, and Spain), 13,000 mT for the British market, 16,000 mT for the Turkish market), with however two slight decreases: the Saudi and Australian markets. Thanks to this strong acceleration achieved partly at the expense of the USA, Dutch results recorded an increase of approximately 30% compared to the pre-Covid period (230,000 mT) (see our additional information at the end of this article). Despite a good performance on the Mexican market, US foreign trade in the sauces sector recorded a significant decline, with volumes in 2021/2022 dropping 14% compared to before the pandemic (350,000 mT).

As for Italy, the world's third largest exporter (12%) of sauces and ketchup, the increase in exports reached just over 11,000 mT (6%) and was the result of an accumulation of measured increases on the British, Polish, Israeli and Russian markets, to name only the main ones. Sales on the French market fell back slightly, after two years of strong increases during the pandemic. The 185,000 mT exported by the Italian sector account for an increase of 45% compared to the average results of the three years of the pre-Covid period (2016/2017 to 2018/2019).

After two years of significant increases, Spanish exports of sauces clearly slowed last year: the progressions recorded for supplies to the Moroccan and British markets did not compensate for the declines recorded to destinations such as Cuba, Australia, Italy, the Netherlands and Germany, the latter two being particularly detrimental to Spanish foreign trade. While the latest annual result of nearly 92,000 mT is down by close on 4,600 mT (-5%) compared to the previous period, Spanish operations over the 2021/2022 period are nevertheless 25% higher than before Covid (around 73,000 mT).

Polish operators exported more than 68,000 mT of sauces and ketchup between May 2021 and April 2022, ranking Poland fifth in the world for this category. Polish trade is mainly carried out within the European Community, where the most significant variations were observed in 2021/2022: increases of several hundred tonnes (Czech Republic, Hungary, Slovakia and Romania) have brought to nearly 2,000 mT the gain recorded in the Eastern EU, along with a marked increase in Saudi Arabia. But more pronounced declines in sales to the Emirates and especially to Germany (-6,000 mT) have resulted in a downward trend (-4%) affecting the dynamics that otherwise featured significant group in recent years. However, the Polish result remains better (+7%) than that of the period preceding the pandemic (approximately 64,000 mT).

By improving its previous performance by more than 20,000 mT, Portugal recorded one of the sharpest increases of the year. Essentially based on sales to the two most buoyant markets of the year (western EU and non-EU Europe), the increase in Portuguese foreign sales (+49%) mainly involved exports to the United Kingdom (+13,000 mT), the Netherlands (+5,000 mT) and France (+2,000 mT). There was no significant decrease in Portuguese activity during the period and the annual result (61,000 mT) was 66% higher than the average activity of the period before the pandemic (approximately 37,000 mT).

According to official customs data, Chinese products saw their exports increase by nearly 22% in 2021/2022, due in particular to significant growth on West African markets (Ghana, Côte d'Ivoire, Benin, etc.) and Hong Kong. The annual result reached nearly 41,000 mT, a level 24% higher than that of the pre-Covid period (approximately 33,000 mT).

Canadian exports are almost exclusively shipped to the large neighboring US market. As mentioned previously, an exceptional increase in the level of operations was recorded over the past year, with sales (36,000 mT) almost doubling between the last two reference periods. For the record, Canadian exports of sauces and ketchup amounted to approximately 8,200 mT before the pandemic.

Comparison of results for the baseline period (May 2021-April 2022) with the corresponding periods for the previous three years (2018/2019 through 2020/2021) and the three pre-Covid years (2016/2017 through 2018/2019).

With the notable exception of the USA and, to a lesser extent, Germany, all countries show an increase in performance compared to the period before Covid.

Trade in 2021/2022 is clearly still marked by the dynamics that emerged during the pandemic. More than thirty months after the beginning of the crisis and after two years featuring an exceptional intensification of trade flows that literally dried up stocks, it seems that the consumption behaviors and the geography of demand that appeared during the first months of the health crisis still remain, while their initial causes – repeated confinements and other forms of restriction – have practically disappeared. Results for 2021/2022 are 8% higher than over the three years preceding the pandemic: perhaps the future will tell whether this crisis has indeed defined a new "steady state" for annual global trade.

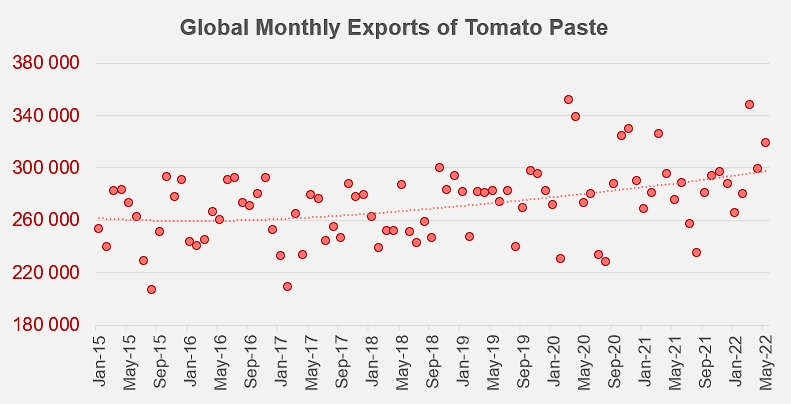

Note: updated data on world trade in the paste category shows that the quantities shipped over the period running June 2021 – May 2022 (3.42 million mT) and the variations observed in relation to the different reference periods are in all respects comparable to those commented on in this report for the period May 2021 – April 2022).

Sauces and ketchup (210320...)

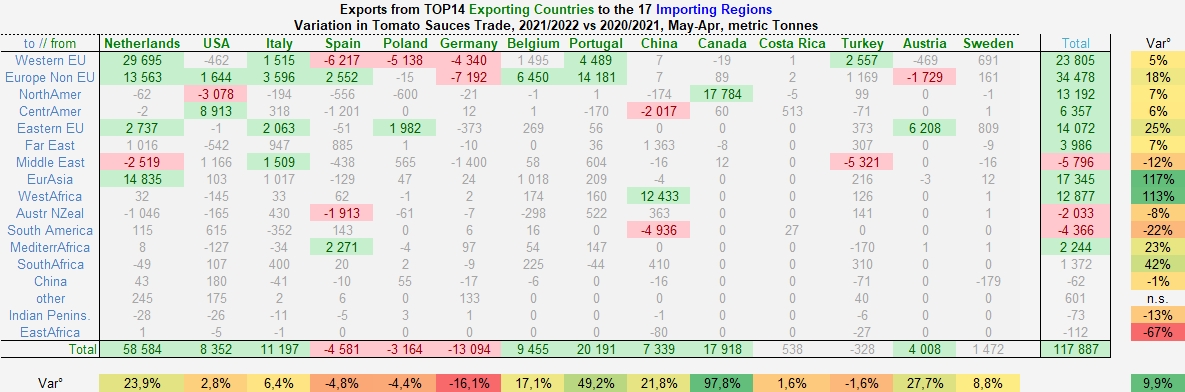

Quantities of tomato sauces and ketchup exported between May 2021 and April 2022 by the fourteen main exporting countries operating in the category, to the sixteen importing regions.

Presentation of 2021/2022 tomato sauces and ketchup sales, for annual trade flows above 1,500 mT.

Recent evolution of the market shares of the fourteen main countries operating in the tomato sauce and ketchup category.

Schematic representation of Tomato Sauces (codes 210320) exports over the period May 2021 - April 2022, from the 10 main exporting countries to the 16 recipient regions.

A detailed breakdown of the 2021/2022 performances for each of the countries mentioned is available on request from the TomatoNews Team.

The monthly trade results (exports, imports, pastes, canned tomatoes, quantities, prices) are published on the TomatoNews website for each of the most important countries in each category. Consult them regularly and be among the first to know!

Find all the topics published under the tag "Trade, statistics, Consumption" by entering the keyword "trade" in our quick and/or advanced article search module.

Source: tradedatamonitor.com