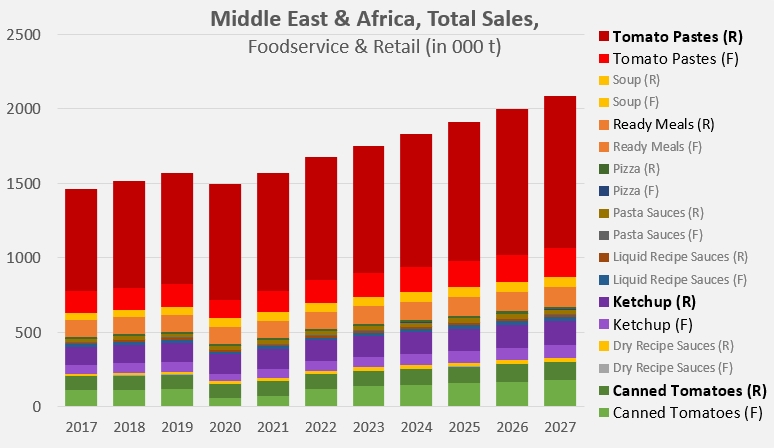

In this market, which is largely dominated by sales of tomato pastes in terms of quantity and value, especially in the retail sector, the health crisis of 2020 led to a sharp slowdown in sales in the food-service sector, particularly for canned tomatoes, ketchup and sauces (liquid and pasta sauces). Despite some increases in retail sales of tomato pastes, soups and prepared dishes, sales momentum in the Middle Eastern and African markets fell back in 2020 to a level just equivalent to that of 2017 (1.46 million t) (see additional information at the end of this article).

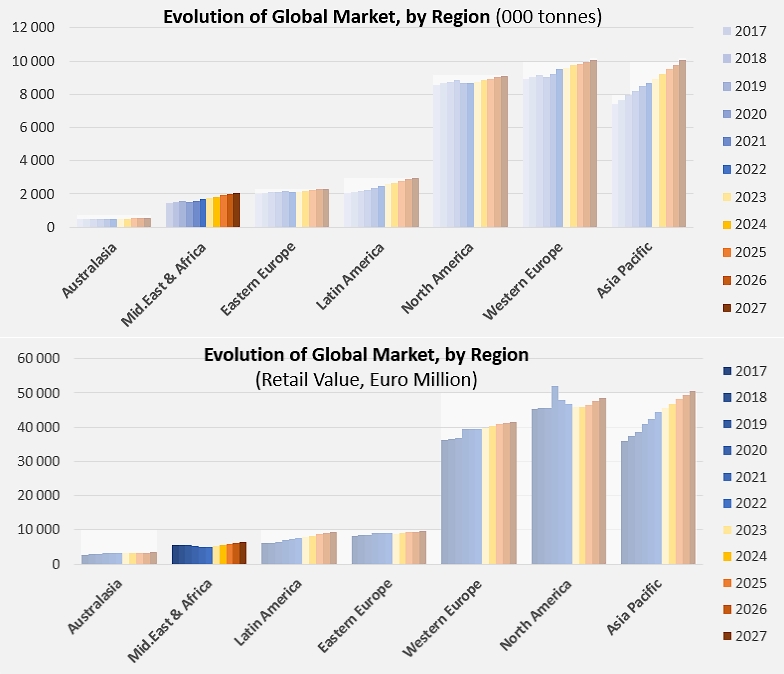

After two years of recovery, the MEA (Middle Eastern and African) market for tomato products (or ranges of products that include tomato-derived ingredients) absorbed 1.675 million tonnes of finished products in 2022, of which 1.31 million tonnes were distributed through retail channels and 369,000 tonnes through the food-service network.

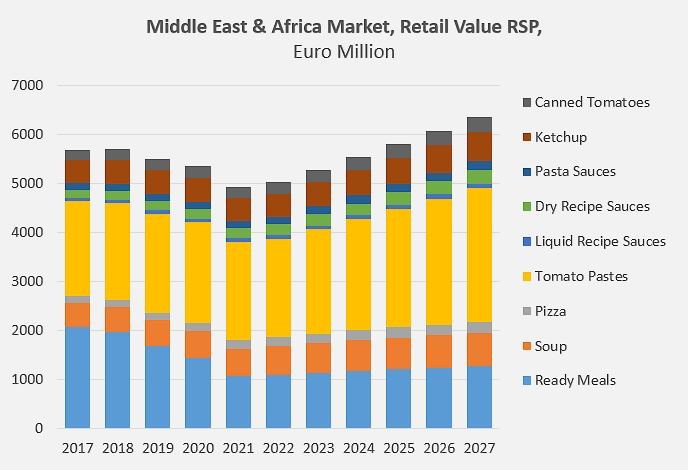

Commercial activity in 2022 was 12% higher in volume than in 2020 (1.49 million t) but, paradoxically, 6% lower in value (retail values only), apparently due to a strong and rapid downward trend in the prices of prepared dishes, prior to the health crisis (see additional information at the end of this article). In fact, Euromonitor forecasts that the value of sales in the retail sector, close to EUR 5.04 billion in 2022, will be the starting point for further growth, taking the value of the MEA retail market to around EUR 6.35 billion in 2027.

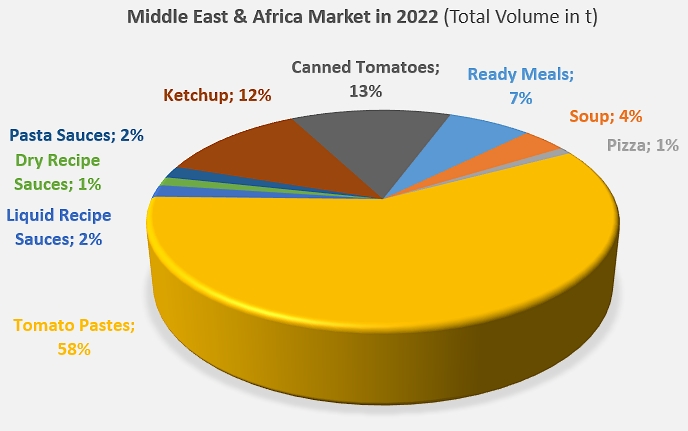

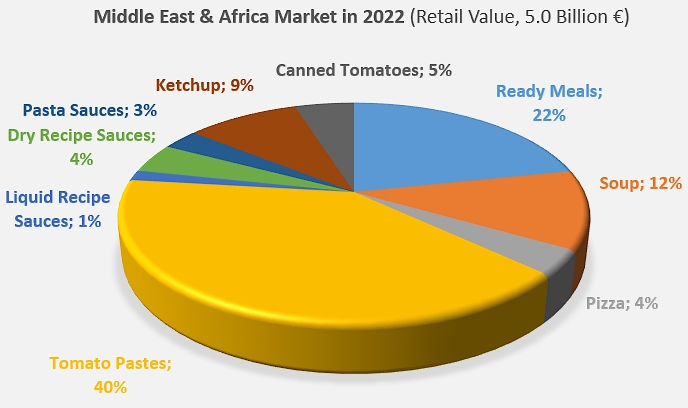

Although they account for well over half of sales volumes (all products combined), pastes accounted for "only" EUR 2 billion of retail spending in 2022, i.e. 40% of total spending on tomato products (or product categories that may contain tomato ingredients) in the retail segment of the MEA market. Despite a significant drop in its value, the second major item of expenditure in this market is prepared dishes which accounted for EUR 1.09 billion, or just under 22% of total expenditure. Soups, with EUR 583 million, and ketchup, with EUR 471 million, complete this group of favorite products of Middle Eastern and African consumers, which ultimately accounted for almost 83% of spending in 2022.

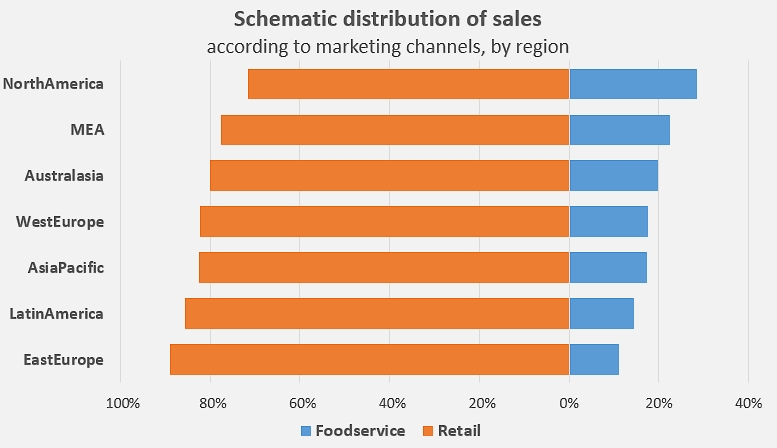

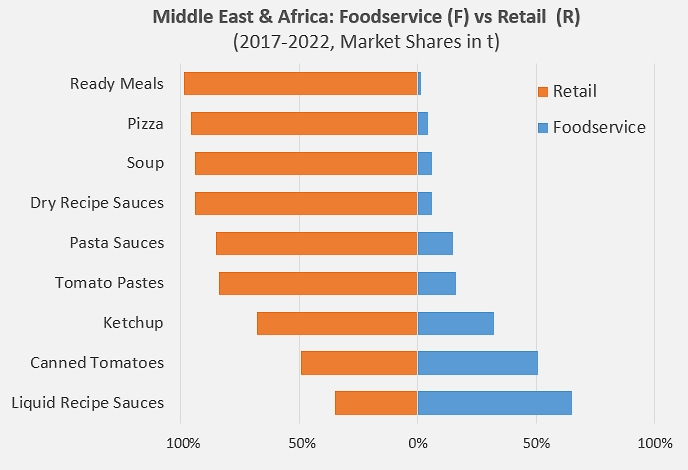

With the food-service sector accounting for just over 22% of sales volumes – and the retail sector for just under 78% – the MEA market is one of the least reliant on retail channels. North America, where over 28% of sales are made in the food-service sector, is the only region to give even greater priority to distributing tomato products (or related product families) in food-service outlets (see additional information at the end of this article).

This schematic distribution masks strong contrasts in terms of marketing channels. In the Middle Eastern and African markets, for example, more than half of all canned tomatoes and almost a third of all ketchup are sold through food-service channels, while ready-meals, pizzas and soups are sold almost exclusively in retail outlets.

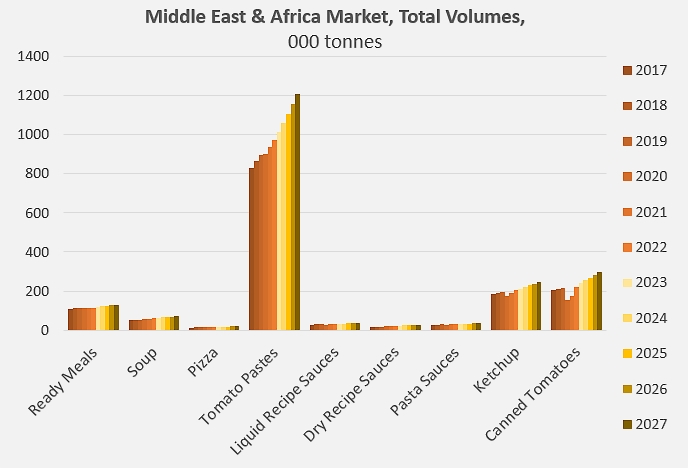

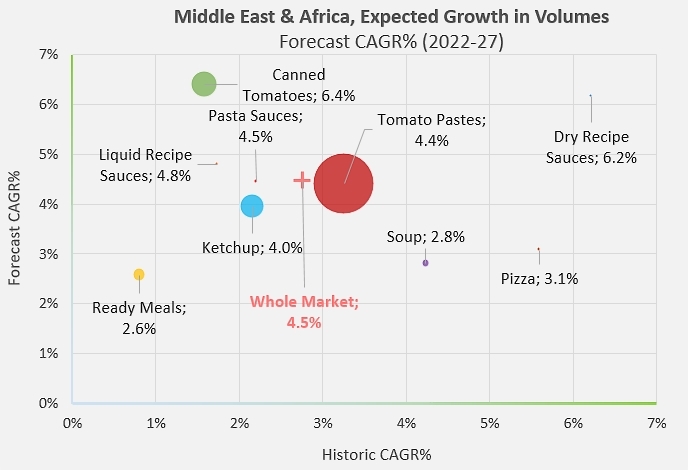

The average annual growth rates (CAGR%) identified by Euromonitor for the MEA market over the 2017-2022 period and even more so over the 2022-2027 period are all positive and above 2.5%. In contrast to what can be observed from time to time for canned tomatoes and dehydrated sauces in Western Europe, or for ready-made meals and soups in North America, all the product families derived from tomato (or which may contain tomato-based ingredients) sold on the MEA market recorded positive growth between 2017 and 2022, and can look forward to consistent development between now and 2027. The three main product categories – tomato pastes, canned tomatoes and ketchup – show growth prospects of between 4% and over 6%. The resulting overall dynamic puts expected annual growth in the MEA market for the period 2022-2027 at around 4.5%, the highest of all the regions studied by Euromonitor.

All markets, studied from the angle of the eight major consumption regions and the nine tomato product families (or product families that may include tomato-derived ingredients) identified by Euromonitor, will be the subject of a summary presentation in the TomatoNews Yearbook 2024, which will be distributed free of charge to participants at the upcoming World Processing Tomato Congress organized by the Hungarian processing industry, next June in Budapest.

Some complementary data

Evolution of total sales (retail and food-service) of tomato products, from 2017 to 2027 (projected figures for the last five years).

Evolution and composition of the value of the MEA retail market for tomato products

Schematic distribution of sales of tomato products (or families of related products) in food-service channels and/or in retail stores, by region

Observed and forecast trends in sales of different categories of tomato products on the MEA market from 2017 to 2027 (projected figures for the last five years).

Evolution of the Middle East & Africa markets in terms of volume and value (retail sales only) and situation in relation to other regions, from 2017 to 2027 (projected figures for the last five years).

Source: EMI International