The tomato markets in Italy and selected EU countries

From the presentation made by Francesco Mutti (CEO, Mutti), during the Tomato News Online Conference held on 17 November 17 2020.

"The first slide is quite a big job that has been done through Nielsen to try and collect all the data from all the European countries.

This exercise hasn't been so easy because all the countries have different kinds of market consideration as in some countries ketchup is included, in others tomatoes sauces, .... In the presentation which we are working on and will present is based on pulp, chopped, cherry, whole peeled tomatoes and else. In fact, everything that is directly related to the previous presentation on the Italian production (see Marco Serafini’s presentation).

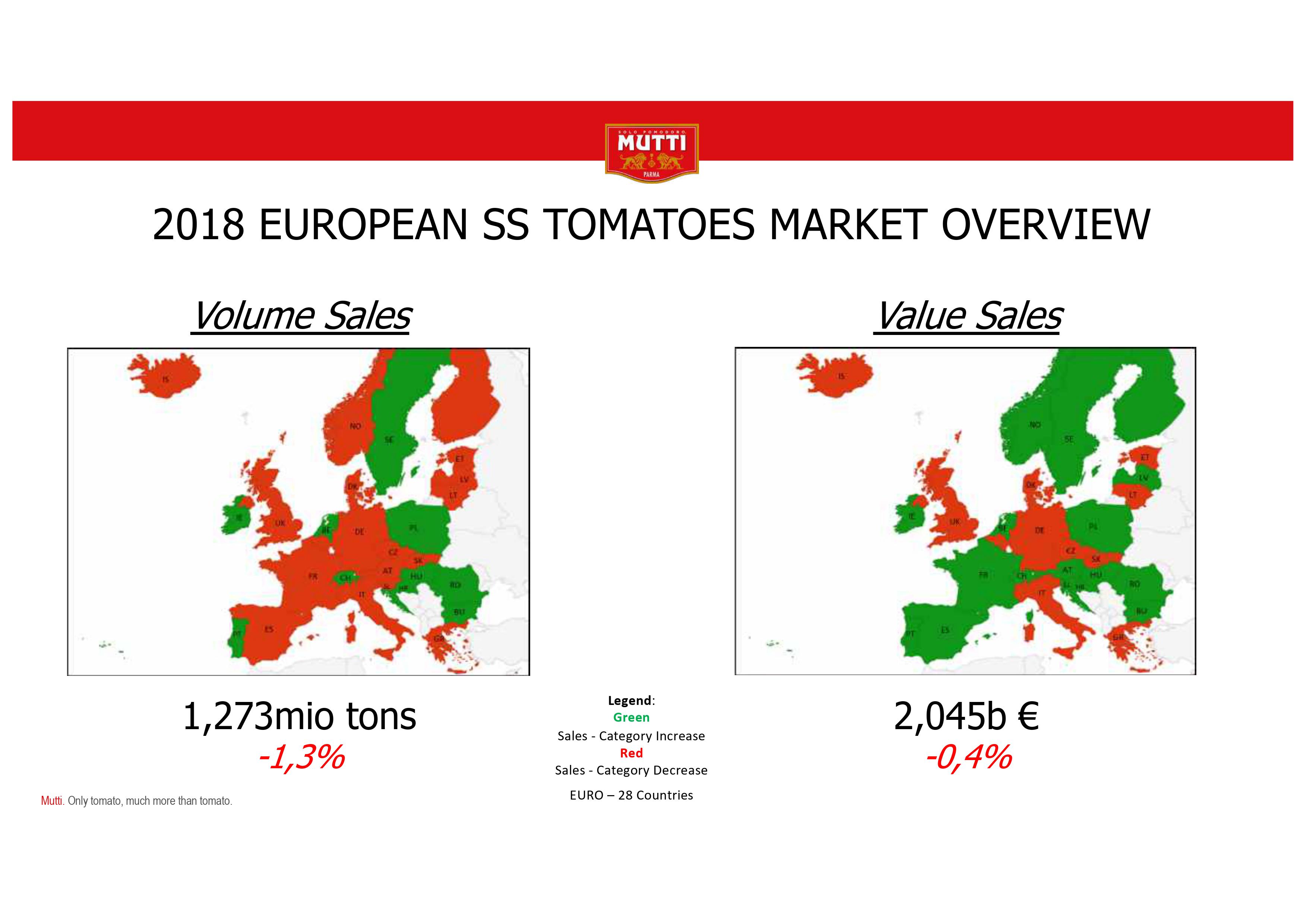

On the slide related to 2018, on the left-hand side you have the consumption in tonnes, so something like 1,27 million tonnes, utilized with a decline of 1.3%. The red countries are the ones presenting a reduction in consumption in volume.

On the right hand-side you see the same categories but in value. So what we can immediately perceive is that in general this is something that the market shows a reduction, but it is stronger in volume than in value.

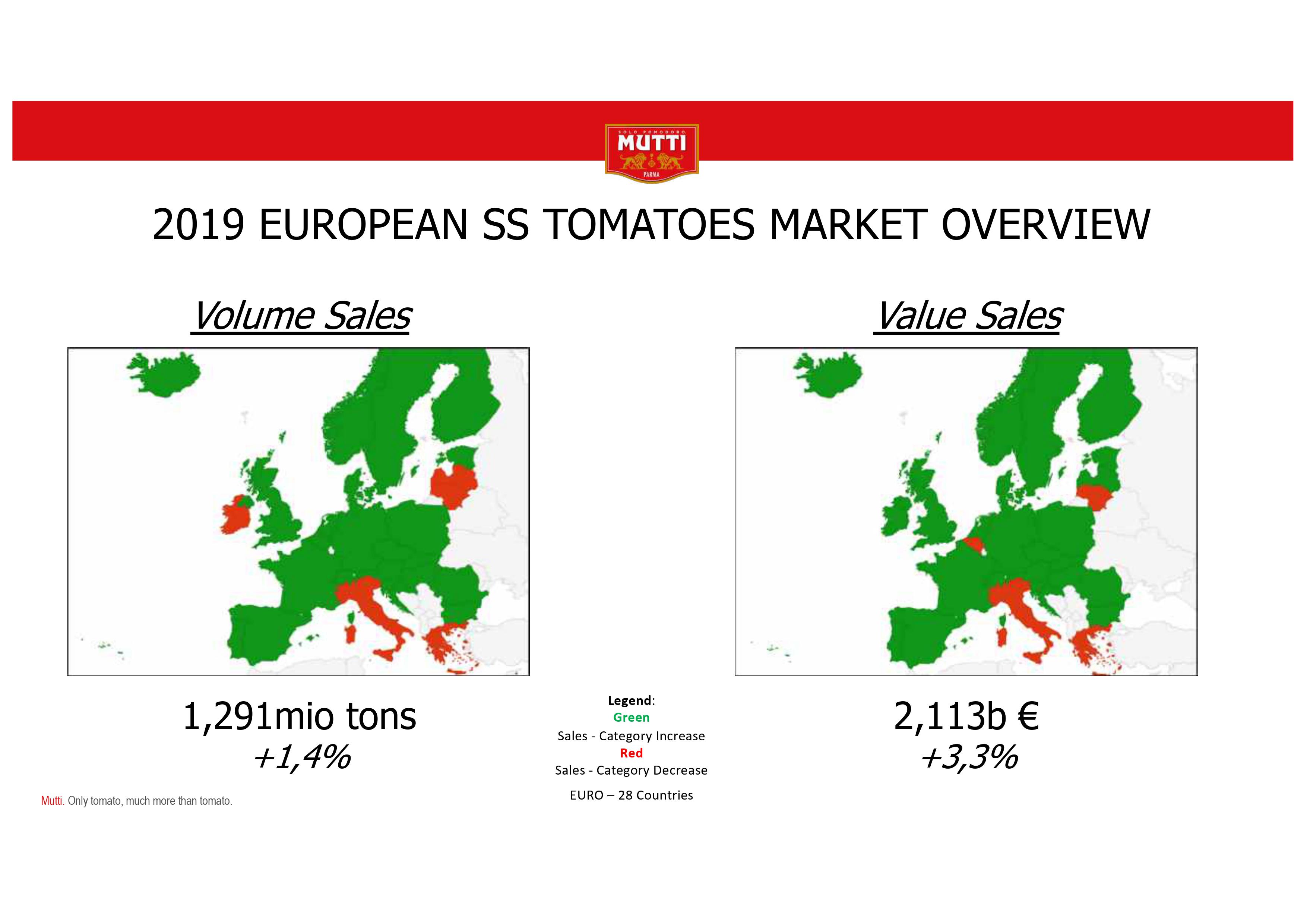

This was 2018. If we go to 2019, unfortunately we do not have this exercise done for 2020, because it takes a few months after the end of the year to have the new data.

There is a significant different approach, so we see an increase, both in volume and in value. It is not clear if this is definitely before the beginning of the pandemic issue, but there's already been a first change in the approach and in the consumption, both in value and in volume. You see that the big red area is the one related to Italy, that is the biggest consumer par head and in total in Europe, so in any case this red part counts much more than the average of Switzerland, Finland or others.

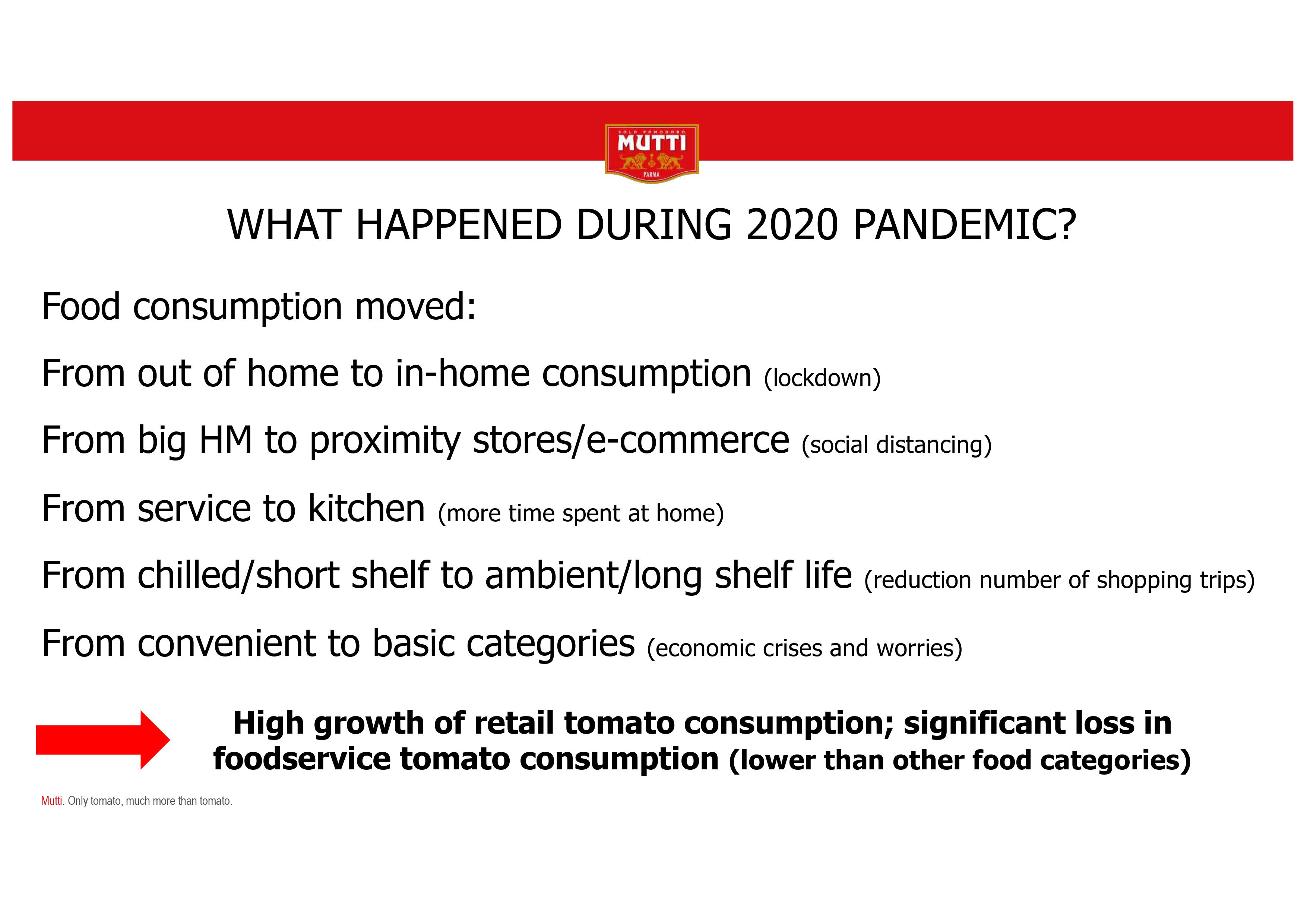

Now, let's enter in some consideration related to the pandemic, so what happened during 2020?

Obviously there have been some big changes. The first one is clearly from out of home to in home consumption, which brings a strong increase in demand, in particular for all the retail products.

Then we move from hypermarkets and supermarkets to much more proximity stores, and e-commerce. Proximity stores are like a relaunch, if you want, of small shops, easier to approach, easier to enter, maybe with a smaller range of products, but in any case, closer to your house, and obviously a very strong e-commerce increase. Also in Italy, which is usually the latest country to have this kind of activity, due not only to the age of the population, we had boom in e-commerce.

Then we move from service to kitchen, so that means related to the time spent in the kitchen by the people that obviously in the lock-down period was much higher, and also a preference given to long shelf-life products. The number of times that the people were going shopping was definitely reduced. A bigger shopping input even if in a smaller supermarket, but with a view to keep the product for longer.

And then a shift from convenient to basic. Basic also in terms of cost.

Obviously, most of these elements were positive for us, because we have a very basic product, we have very cheap products, and very often you need sometimes to cook tomatoes.

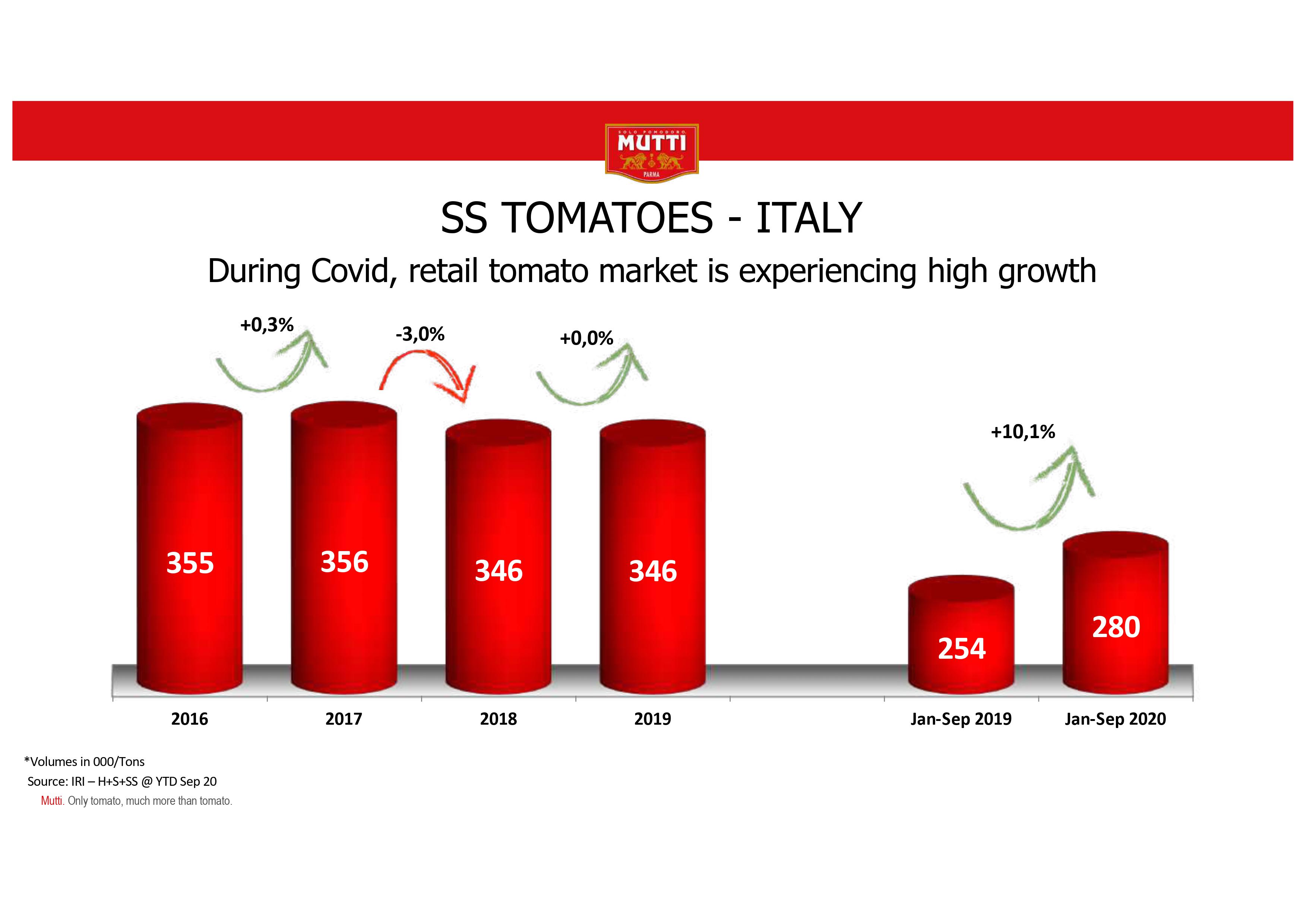

Now we go to a short deep dive in some of the major markets, we start with Italy.

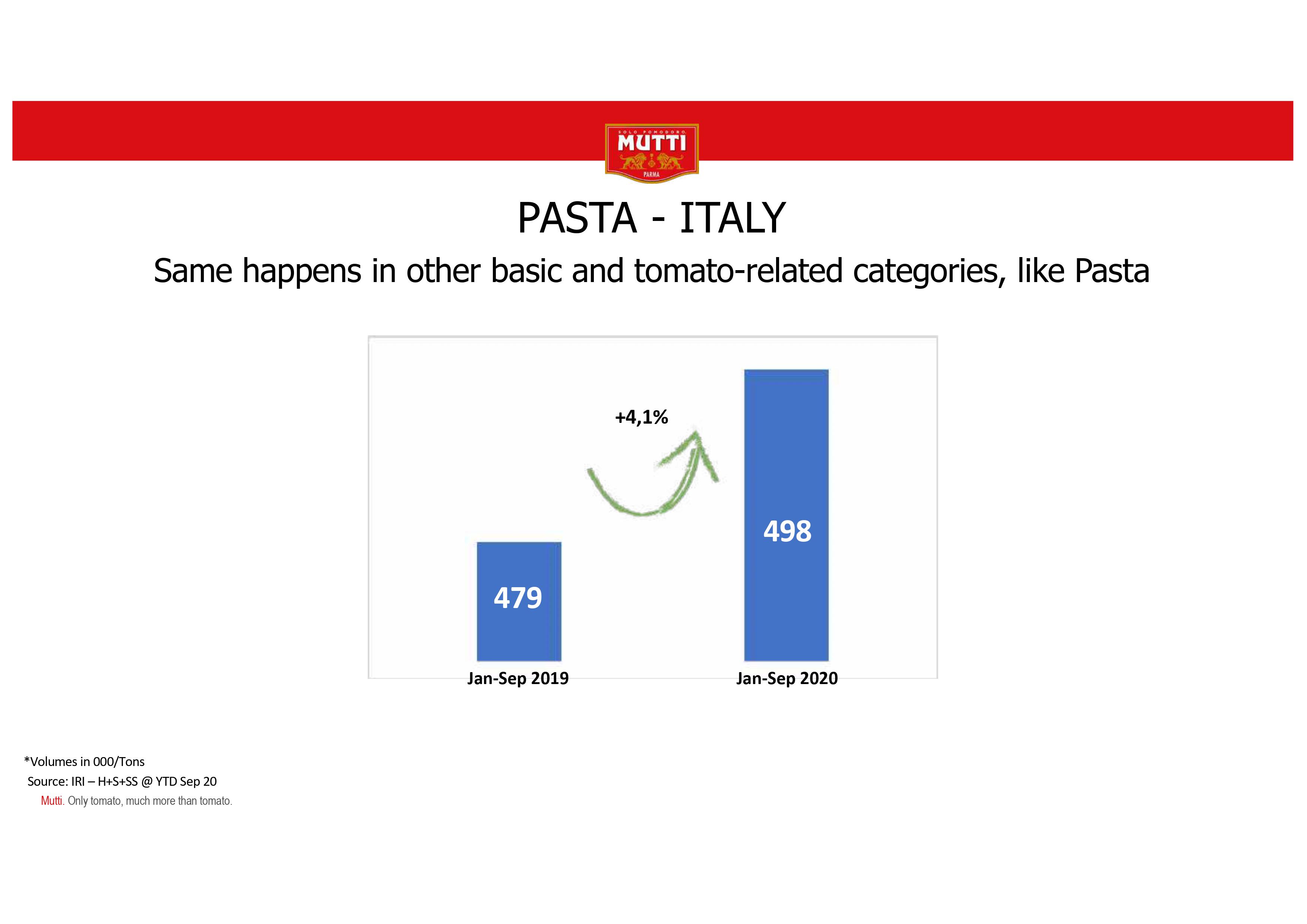

In Italy, you can easily see how from a slight decline in market of 3% in 2017 versus 2018 counts a lot, versus a zero that looks like a red, but then in the first 9 months of 2020 we had an increase of 10% in consumption, which is totally unexpected and totally out of our categories. The same happened basically in another category, if we can move to the next one, which is pasta.

So, also pasta, not with the same dimension, as for tomatoes, had a very strong increase in a market that had been strongly declining for ages. What does this mean, why did I put pasta? Because it shows that the consumption of tomatoes moved from its natural position that was very linked to pasta to something else, probably a lot of pizza. So consumption of pizza at home was really important, has been extremely important.

So, also pasta, not with the same dimension, as for tomatoes, had a very strong increase in a market that had been strongly declining for ages. What does this mean, why did I put pasta? Because it shows that the consumption of tomatoes moved from its natural position that was very linked to pasta to something else, probably a lot of pizza. So consumption of pizza at home was really important, has been extremely important.

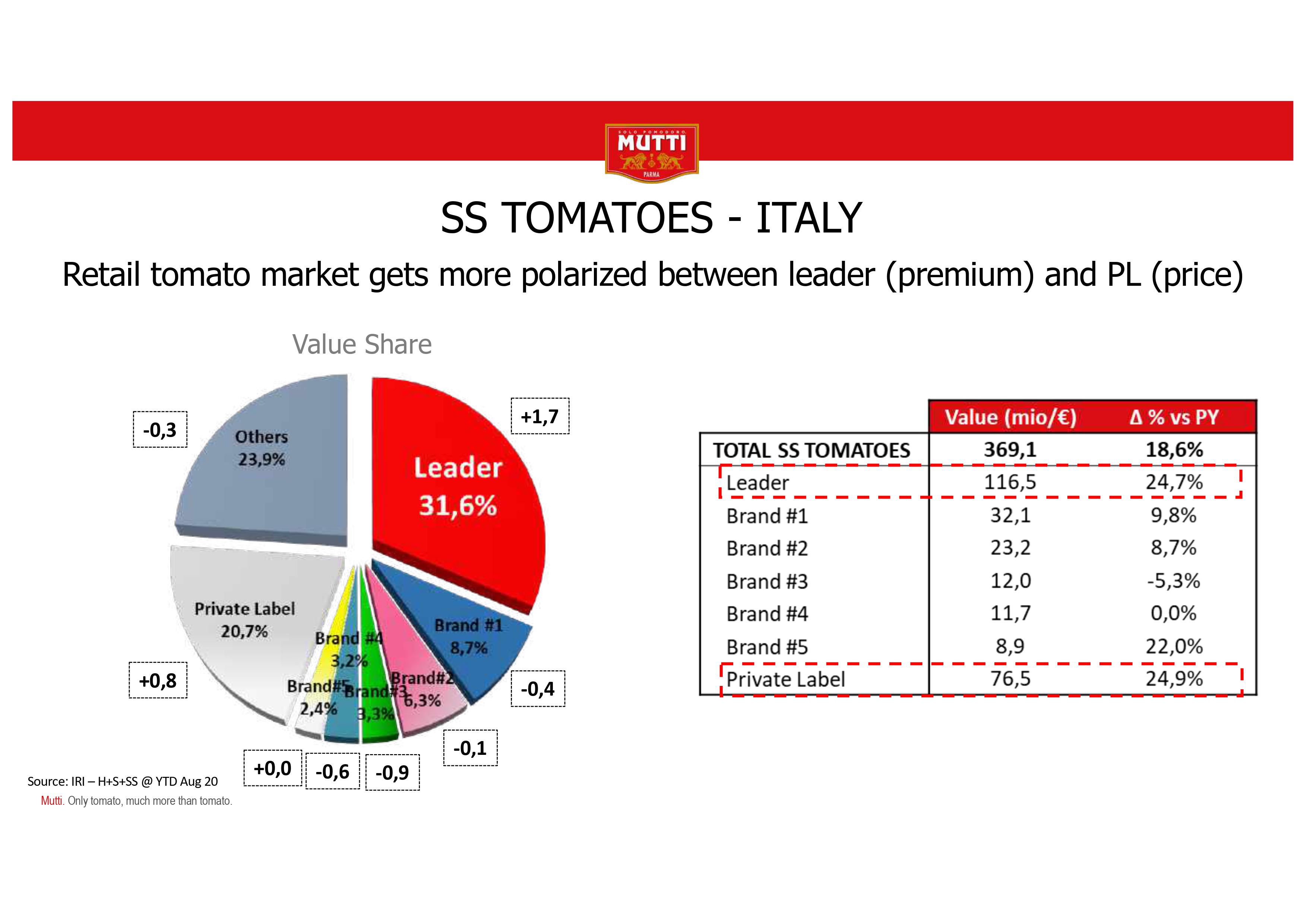

Again let's see in a few markets where we can see, for example in Italy, a strong polarization versus both the leader of the market and the private label. Basically the driver for this has been the fact that entering to a supermarket during the Covid was not such a pleasant experience, so the time and the pressure and the need of finding something that gives you a certainty, rather than looking for new products, and looking for development of new products. As a company, we can say that the launch of new products in 2020 has been much tougher than in the past. You couldn't have supporters, you couldn't have hostesses in the points of sales, so there were many elements that reduced the capacity of launching, and the level of attention of the consumer was much lower than on average. And already into the red sector it's not huge.

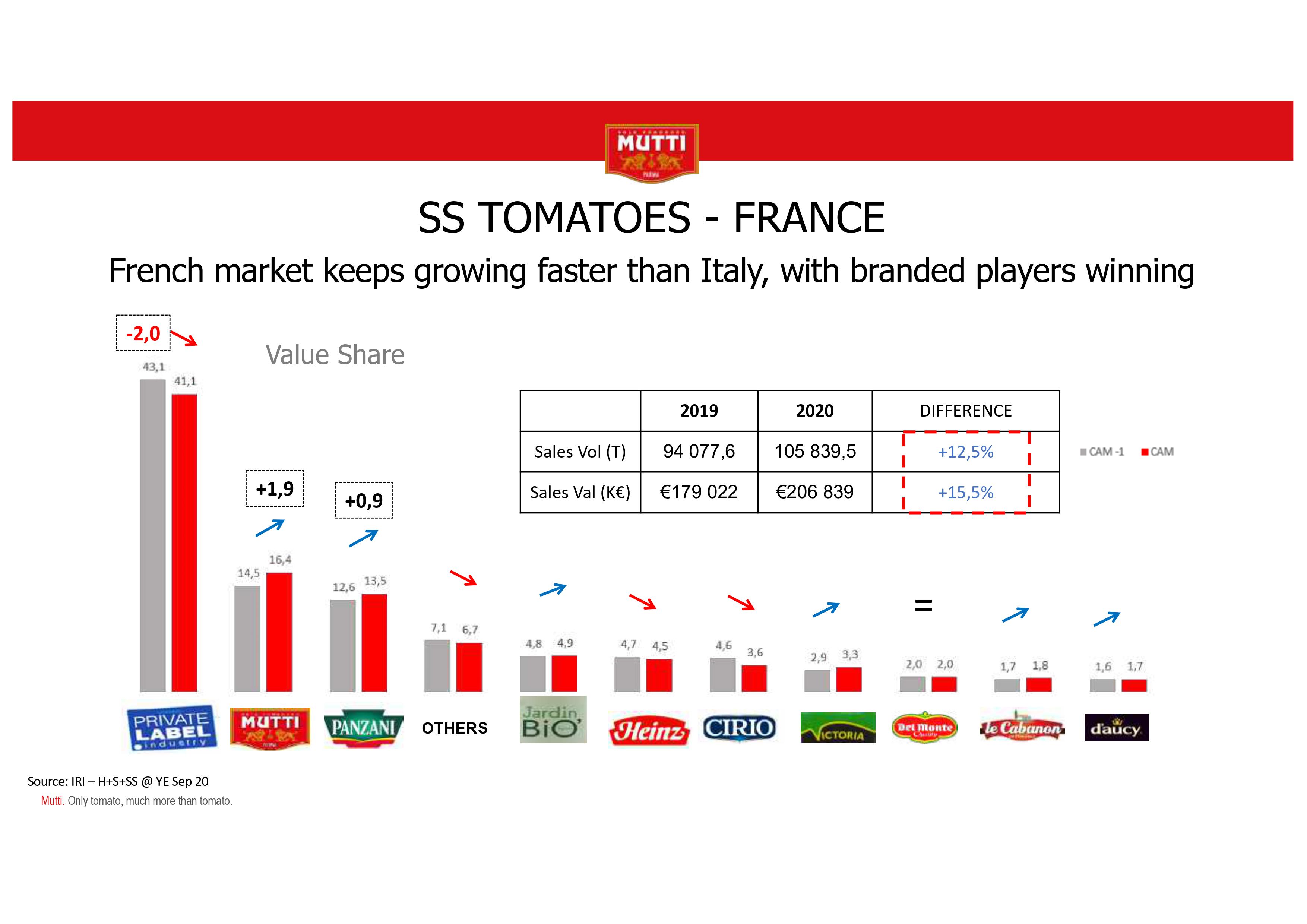

Moving to the French market

There are also the brands we collected from different areas. Here we see the growth again of the main players and we have a decline in private labels. But this decline in private labels in France came from different elements. The first one is the dimension of the private label, that is not considered as natural as it should be, so, private label should count for something around 30-35%. The French market had a very strong level of private label intensity.

The other point was that some private labels ran out of stock during the period of May-July of this year.

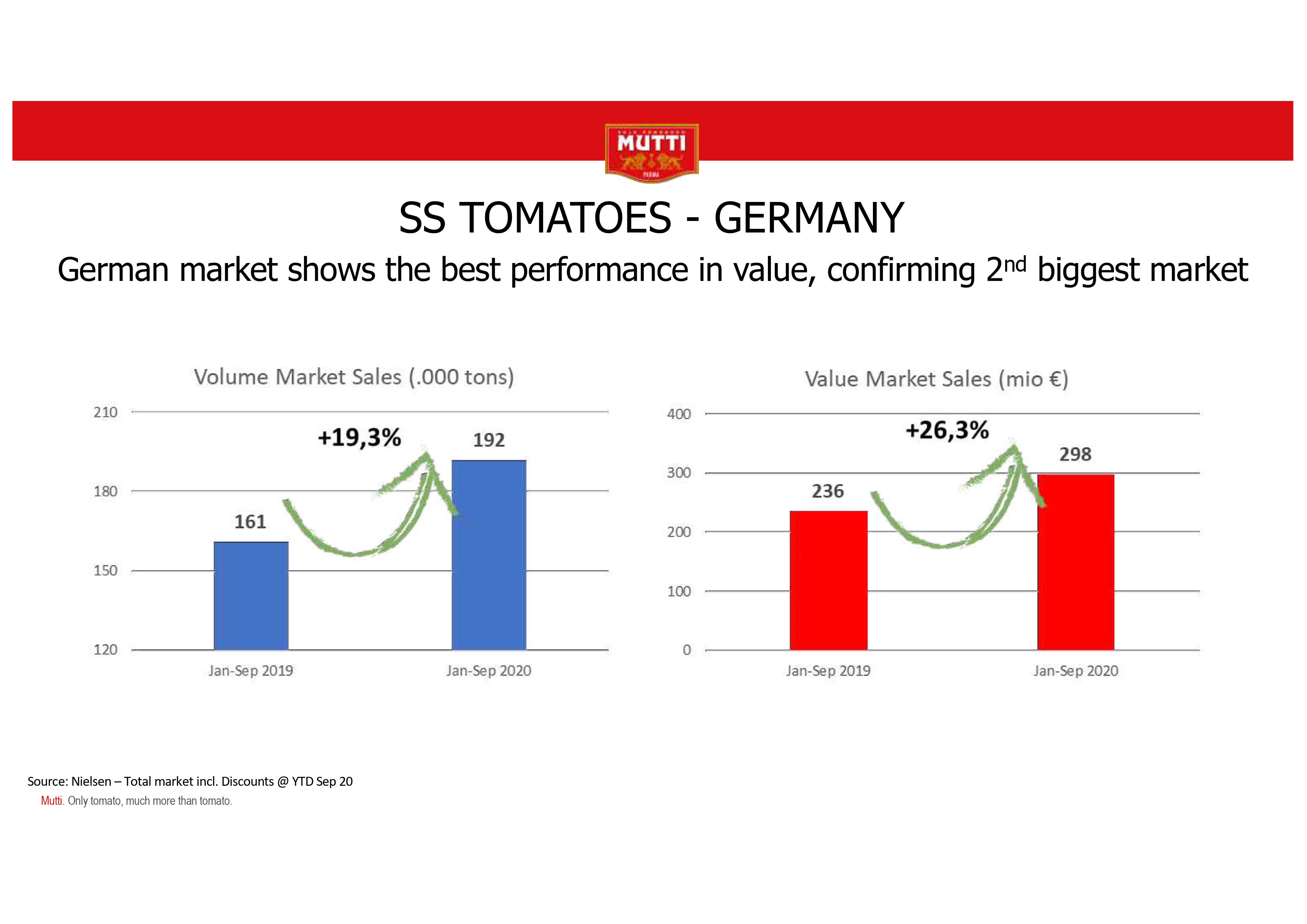

If we move again, to Germany, another very big market, unfortunately we do not have much.

In Germany we see a very strong market development. So really there has been a change, less in volume but in value with a growth of 20%. The average of the German market was a slight decline in the last three years.

There has been a change in this, also in communication and advertisements that started something like three years ago and that gave a new life to the tomato market and so, also the previous years were slightly positive.

But nothing to see when we are talking about a couple of points of growth, here we are talking about a 20% growth. Totally unexpected.

Again, we see that the growth in volume is much smaller than the growth in value. Why? In general, in all the markets, there have been more elements. A part of it is explained by the leader, so something that you trust, or you know already. A second element was a strong reduction of promotions, not in all the markets, but there has been a reduction in promotions. The third element has been the pressure given by the consumer so when shoppers were in the point of sales, they were less careful about the promotions. They knew what they were looking for, they were into what they were used to, more than new products, and that gives these 6 points of growth, from volume to value.

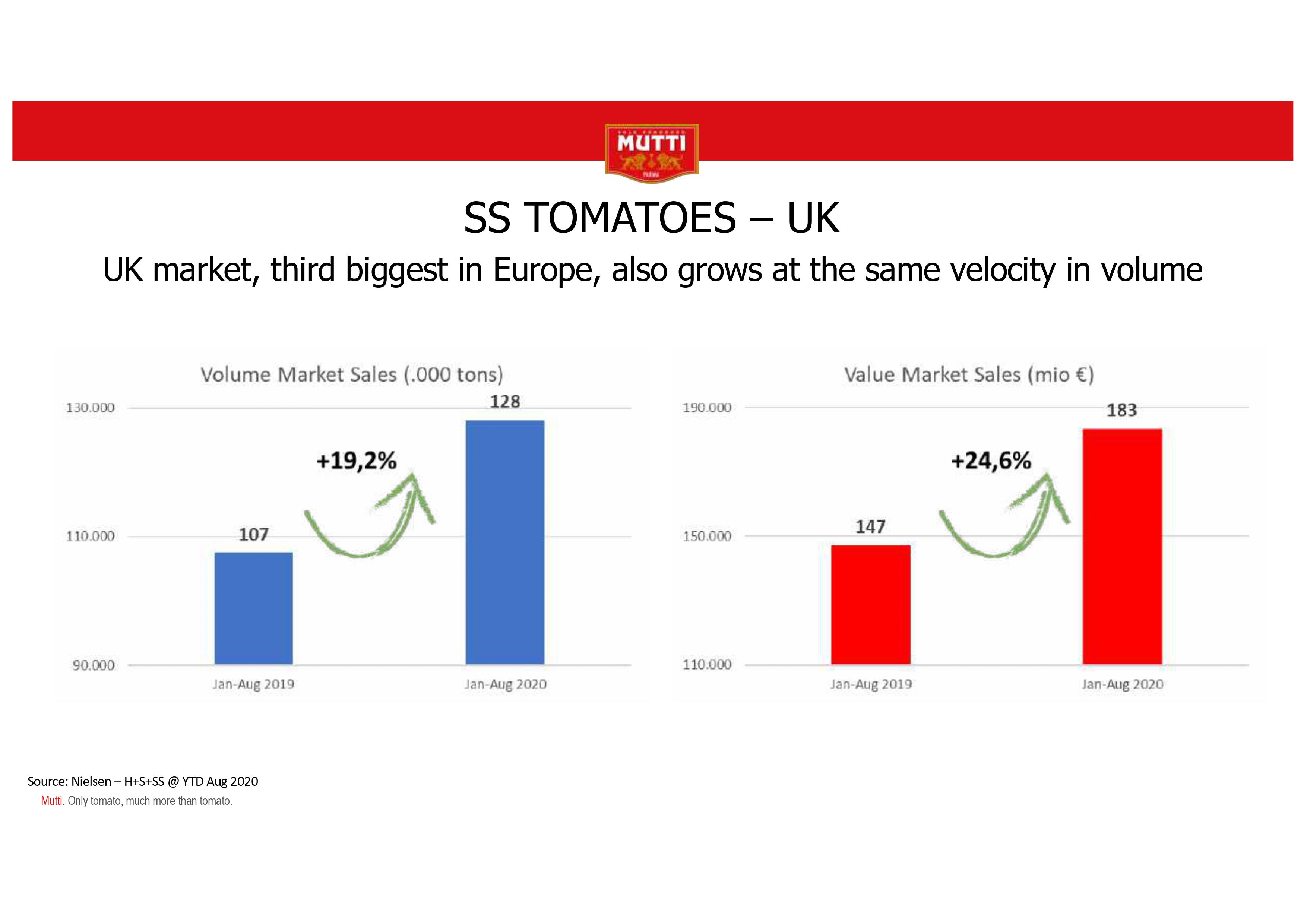

Also the UK market had basically the same result.

Again, a very good, astonishing growth in volume but the best performance has been in value. In general, if we think of a long-term perspective we see that the market is going more and more with a decline in terms of volume, which is sustained in a better way by the value, through differentiation. Marco was mentioning a few minutes ago the growth of cherry tomatoes, that could be also datterini… that would be Pomodoro del Piennolo. All of these definitely have a completely different euro per ton or per kg versus passata or also normal chopped meat. The other element is also the downsizing of the dimension of the jars, in general the size bought by the consumers is the can.

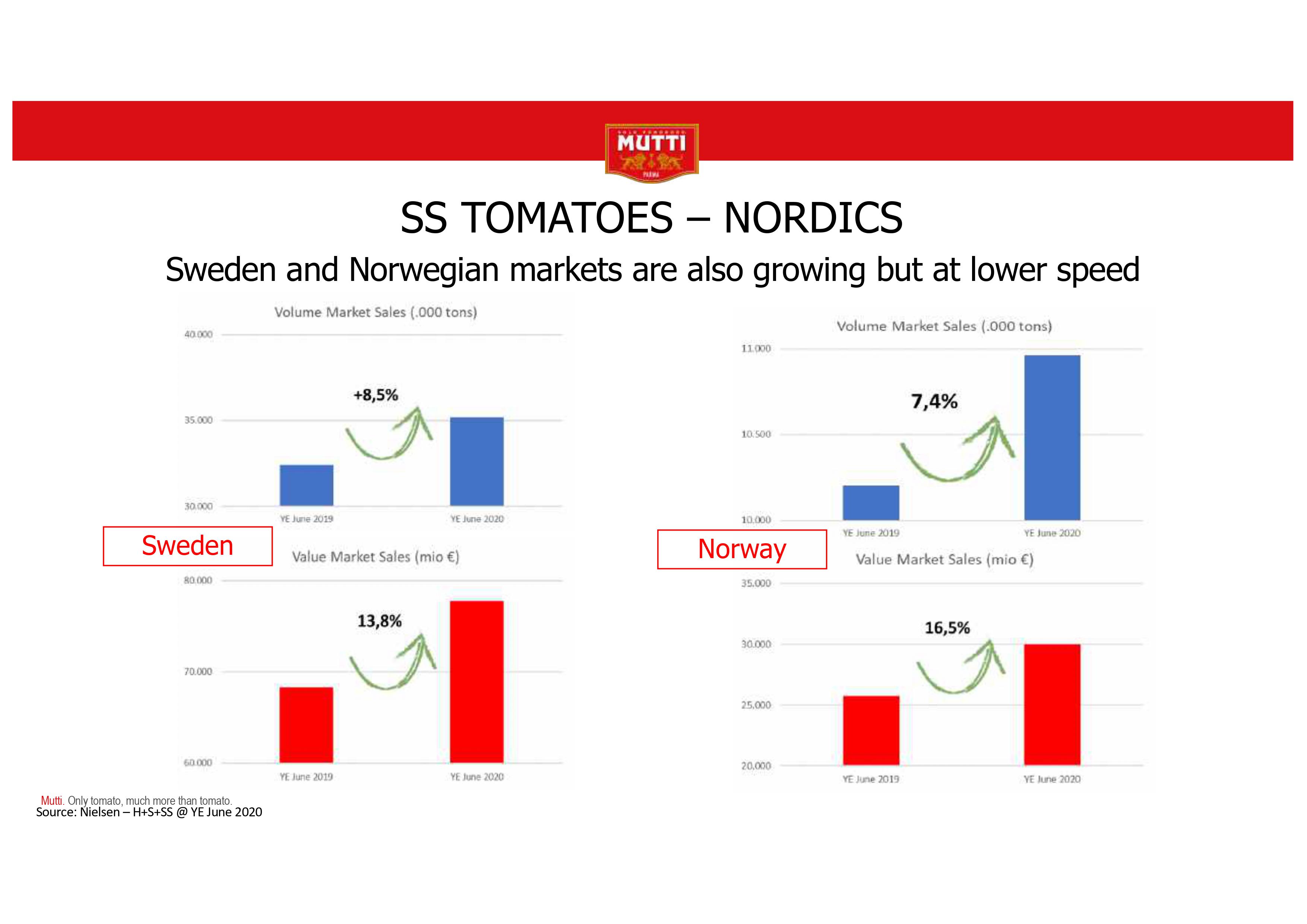

So this is the latest in this market, it's Nordics, with a couple of countries, Sweden and Norway.

Here the increase is a little bit less but still very important, considering that both those countries, Sweden never went into a real lockdown, I don't know exactly for Norway, I think Norway did some but not as strong as we had in Italy or in France or in other countries. But in any case, even here we have a strong increase and again an increase that is more in value than in volume.

Following this a short evaluation, the big question is: what's next?

We should, hopefully, be out of the pandemic within a few months. Hopefully...

What will remain and what will change? It is very hard to say and if you knew it, well, you could bet a lot of money.

Definitely the e-commerce will be established. There are many different ways of considering e-commerce. In France, it's driven a lot by drive-through in which you do your shopping on the web and you go to the point of sales to collect it, this new way of delivering products boomed, in Italy and not only, like "supermercato 24" which is an Italian example, not only they play also in another couple of countries in which they charge you a percentage of what you buy and they deliver it at home. You can choose the supermarket or else, you ask them to do your shopping and they bring it home.

The big question is definitely: What will happen in the home consumption. Why? They will be a moment in which, hopefully again, the Covid will finish. We think that, at that time, there will be a beginning of "coming back to normal". Meaning we will start going out again, having dinner with friends, but we think that the working from home, the smart working, will remain established. There has been a step change during this period. So, we do not expect that the number of people going to the office every day will come back to normal, even when the pandemic is finished. That will shift partially the consumption from out of home into home consumption.

Then the question is: but if you are at home, at lunch, you want to go out, have a sandwich or stay at home and have pasta, maybe with your wife or else, at home.

In any case what we expect is an acceleration in coming back to the new normal but not reaching the same level as at the end of 2019 for a certain number of years. It is not here but there is an unbelievable graph that shows how the two categories, in home and out of home, they just cross a few years ago and now they come back to 25 years ago in terms of consumption. They are the new normal, but in any case, we gradually come back to what is convenient so people will have less time to invest at home when the lockdown will be finished and probably will come back to consumption of chilled and in any case shorter life versus other categories of product.

So in any case the big question is really: What will change in the future after the pandemic between in house and out of home consumption?

Thank you for your attention".

Most of other presentations from the Tomato News Online Conference will be transcripted during the coming weeks but all slides are already available here. The videos of all the presentations will also be released in a few weeks (they are for now reserved for the webinar attendees).