Exports are increasing and domestic consumption is picking up

The operating results that we have published in recent months for volumes and revenue stemming from the worldwide trade in tomato products, particularly for the Italian industry, have shown a clear upturn in Italy’s foreign sales and underlined the exceptional position occupied by this country in economic terms within the context of the worldwide industry.

The operating results that we have published in recent months for volumes and revenue stemming from the worldwide trade in tomato products, particularly for the Italian industry, have shown a clear upturn in Italy’s foreign sales and underlined the exceptional position occupied by this country in economic terms within the context of the worldwide industry.

At the beginning of June, new information recently published by the ISMEA confirmed these trends that we already identified with regard to foreign trade, adding to the early signs of recovery by demonstrating an upswing in consumption on the Italian domestic market.

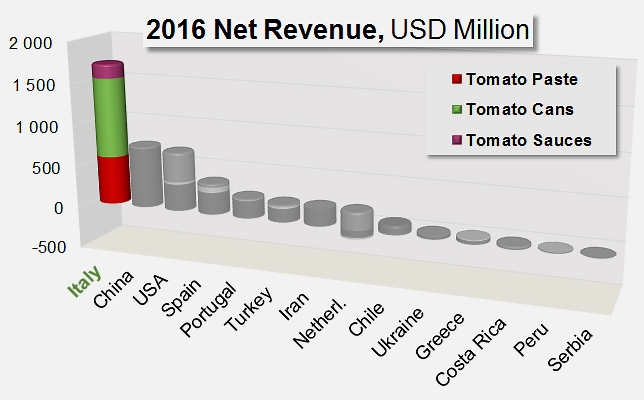

According to data compiled by the Services Institute for the Agricultural Food Market, the total turnover of the Italian industry amounted last year to EUR 3.2 billion (approximately USD 3.5 million), including slightly less than half of which came from foreign markets. The ISMEA has pointed out that Italy is the world's biggest exporter both for pulped tomatoes and for peeled tomatoes (with a 77% share of this last category on the worldwide market, ahead of Spain, which holds 8% approximately, and the United States with 4%), but also for passata and pastes (with 26% of the worldwide turnover for this last category in 2016, closely followed by China whose trade accounted for 25% of the total figure last year).

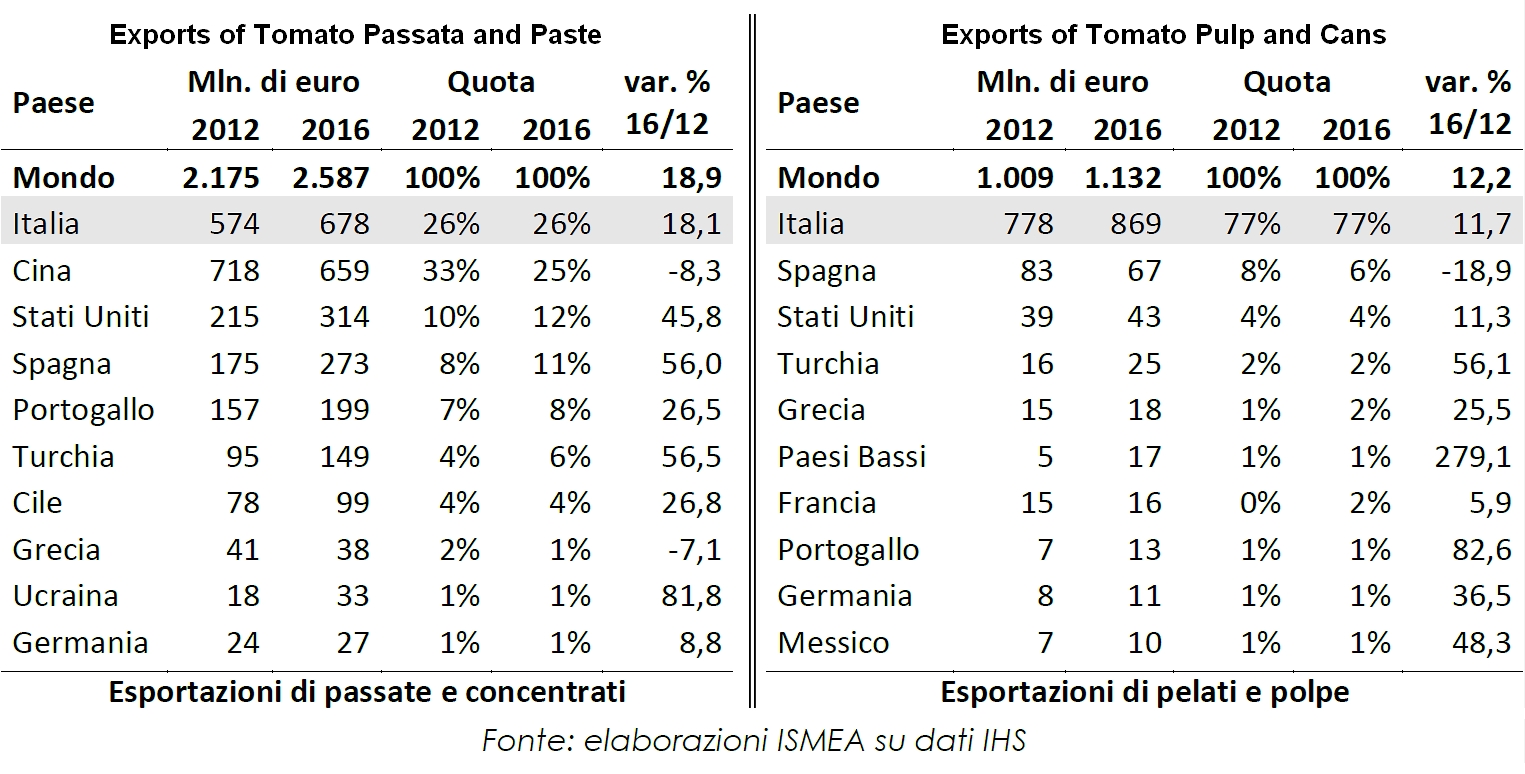

The world's main exporters of tomato products (value, market share and variation) 2012/2016

Among other important points, the report pointed out that from 2012 to 2016, Italian exports of pulped tomatoes and peeled tomatoes increased by 12%, slightly more than those of the United States (11.3%), while Spain's foreign sales recorded a sharp downturn for this category (-18.9%). As for passata and pastes over the same period, the ISMEA reported an 18% increase in tomato exports, well below the increase recorded by the United States (+45.8%), but which should be interpreted in light of the notable drop in performance of the competing Chinese industry (-8.3%).

Domestic market: the end of a decade of decline

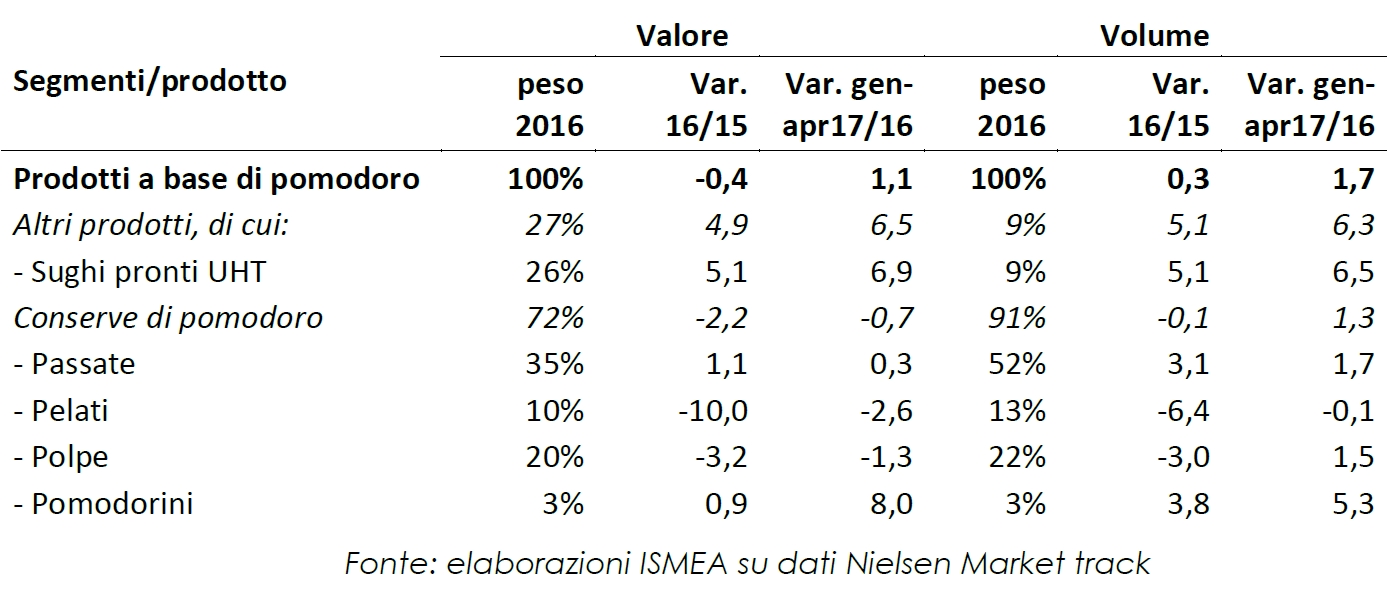

Along with this recovery in export trade, the ISMEA report, based on Nielsen data, pointed out that the 2016 marketing year put an end to an entire decade of regular and continual decreases in the retail sales of tomato products. The indicators remain cautious, with sales of tomato products remaining globally stable in terms of volume (+0.3%) and in terms of value (-0.4%). Yet within the sector, a number of product categories recorded a sharply increased performance, like ready-to-use sauces (26% of the total turnover for the category), whose sales have increased by 5.1% both in terms of volume and value. Similarly, retail sales of passata grew 1.1% in value and 3.1% in volume, while sales of canned cherry-tomatoes also increased by 0.9% in value and 3.8% in volume.

Even more telling than the 2016 results, available data for the first four months of 2017 has confirmed this reversal in the market trend, with an increase of 1.7% in the volume of sales and 1.1% in the value of the category overall.

It is however important to note that the slowdown in consumption for the peeled tomato and paste categories has not enjoyed the same evolution, with 2016 results down by 10% in value and 6.4% in volume compared to 2015 for peeled tomatoes, and down 3.2% in value and 3% in volume for pulp.

Appendices/Annexes